Introduction

In India, RegTech, or Regulatory Technology, has moved from being a buzzword to a backbone of financial integrity. With regulatory scrutiny higher than ever and digital ecosystems expanding fast, the demand for compliance-driven technology is now at an all-time high.

RegTech is the unsung hero behind the smooth digital banking, Digital KYC, and anti-fraud mechanisms we now take for granted. It doesn’t make loans or open accounts like a fintech app does. Instead, it ensures every transaction, identity, and document follows the rules automatically. This blog will guide you through everything about RegTech—from its definition and technologies to its applications, industries, and distinctions from FinTech.

What Is RegTech?

RegTech refers to the use of technology to help organisations comply with laws and regulations efficiently, accurately, and transparently. It employs technology-driven solutions that automate, simplify, and strengthen compliance management. This technology merges software, data, and analytics to monitor, report, and predict compliance obligations in real-time.

The term first appeared after the 2008 global financial crisis, when regulators worldwide tightened controls to prevent fraud and systemic risk. Financial institutions found traditional compliance, which comprised manual audits, paperwork, and checklists, to be too slow and expensive. Technology became the natural solution.

Why The Need For RegTech?

Every regulated industry faces three constant challenges:

- Complex regulations that change frequently

- Heavy penalties for non-compliance

- Mounting operational costs for manual checks

RegTech addresses all three by turning compliance into a proactive system. Instead of waiting for auditors to find errors, firms can detect them instantly through AI models, dashboards, or automated alerts. Consider RegTech as a vigilant digital assistant sitting inside a company’s IT system. It reads rules (like the RBI’s KYC guidelines), compares them with ongoing business data (transactions, identities, documents), and flags anything that doesn’t fit. The same system can then produce regulations-ready and extremely accurate reports without any human spreadsheet juggling.

The Technologies Behind RegTech & Its Working

At the macro level, RegTech is an entire ecosystem. It makes use of the combination of data science, automation, and secure computing to create an always-on compliance framework. Each technology contributes to a wider framework often called RegOps or Regulatory Operations, which keeps financial institutions compliant with regulations. Here are the key technologies powering RegTech:

Artificial Intelligence and Machine Learning

Artificial Intelligence (AI) and Machine Learning (ML) sit at the centre of every mature RegTech stack. In India, AI-driven models help banks and NBFCs detect AML transaction typologies such as placement, layering, and structuring across payment rails like UPI, NEFT, and IMPS. Instead of flagging random alerts, modern systems apply behavioural scoring and entity resolution to connect related accounts and identify real risk.

- ML algorithms continuously learn from past suspicious-activity reports, improving detection accuracy.

- AI-assisted sanction-screening engines match customer names against fuzzy or partial entries across UN, OFAC, and domestic lists.

- Predictive analytics help estimate the probability of non-compliance based on transaction patterns, geography, or product type.

Natural Language Processing

The pace at which RBI, SEBI, and IRDAI issue circulars makes manual tracking impossible. Natural Language Processing (NLP) addresses this by teaching systems to read, interpret, and summarise regulatory text automatically.

Compliance teams now rely on regulatory-intelligence platforms that parse circulars overnight, extract relevant sections, and map them to internal policies. Some advanced tools even employ semantic comparison models to show clause-level changes between old and new guidelines.

Robotic Process Automation (RPA)

RPA acts as a bridge between compliance policy and operational delivery. Bots handle routine, rule-based work: collecting KYC documents, validating PAN–GST combinations, reconciling account data, and filing STR/CTR reports to FIU-IND.

When the volumes become large, RPA operates alongside workflow orchestration tools so that exception handling is escalated to human reviewers while the rest of the pipeline runs autonomously. The result is higher throughput, lower operational risk, and near-zero manual data entry.

Big Data and Advanced Analytics

Data is what RegTech platforms thrive on. They integrate feeds from core-banking systems, loan origination platforms, payment gateways, and CRM tools. Using stream-processing engines and distributed data lakes, they can monitor millions of transactions in real time.

These analytics help identify emerging risk clusters, predict defaults, and help quantify exposure for internal risk committees. Dashboards powered by self-service BI tools give compliance heads near-instant visibility across branches, products, and geographies.

Blockchain and Distributed Ledger Technology

Few technologies inspire as much trust as a distributed ledger. In RegTech, Blockchain ensures that compliance records are immutable and verifiable.

India’s ongoing pilots under the RBI’s Regulatory Sandbox Framework explore shared KYC utilities where banks can access a verified customer profile once it’s approved by any other regulated entity. This model reduces duplication while maintaining complete traceability under customer-consent protocols.

Cloud Computing, Microservices, and APIs

The cloud is what makes RegTech scalable. Modern solutions are built as cloud-native microservices, allowing banks and regulators to process compliance enforcements securely and at scale.

- Most RegTech providers host their services on compliant local data centres in Mumbai, Hyderabad, or Chennai to satisfy data-localisation norms.

- Open APIs power instant verifications — from pulling CIN and DIN details via MCA to checking e-sign validity through NIC or UIDAI gateways.

- API gateways with JWT-based authentication and TLS 1.3 encryption ensure inter-institution data exchanges meet RBI’s cybersecurity directives.

Cloud adoption also enables SupTech (Supervisory Technology), where regulators themselves use cloud-based dashboards to monitor reporting entities in near real time.

Optical Character Recognition (OCR) and Computer Vision

Document authenticity remains a key metric for compliance. OCR extracts data from physical forms, while computer-vision algorithms detect forgery, tampering, or mismatch.

During Video KYC processes, OCR reads identity details from an Aadhaar or passport; facial-recognition models confirm liveness and match the applicant to official records. Both these tools, combined, have made remote customer onboarding both regulatorily compliant and operationally viable in India.

Knowledge Graphs and RegData

Financial crime hardly ever occurs in isolation. Knowledge graphs help visualise the relationships among different entities like directors, shareholders, subsidiaries, vendors, and politically exposed persons (PEPs).

By integrating data from MCA, stock-exchange filings, and sanctions databases, RegTech platforms can automatically expose beneficial-ownership overlaps or undisclosed connections between borrowers and suppliers — critical for corporate due diligence and third-party risk assessment.

Cybersecurity and Encryption

Every RegTech process involves sensitive information. With the Digital Personal Data Protection Act, encryption, consent management, and data retention governance have become mandatory duties.

Industry-grade RegTech platforms employ:

- AES-256 encryption for data at rest and TLS 1.3 for data in transit.

- Zero-trust network architectures with adaptive access control.

- Immutable audit logs for regulator-verified trails.

Applications Of RegTech

Consider compliance synonymous with a human being; RegTech would be its nervous system, responsible for sensing, interpreting, and responding instantly to regulatory signals. Over the past decade, its applications have expanded from simple KYC checks to full-scale governance, risk, and compliance (GRC) ecosystems. Let’s look at the applications of RegTech:

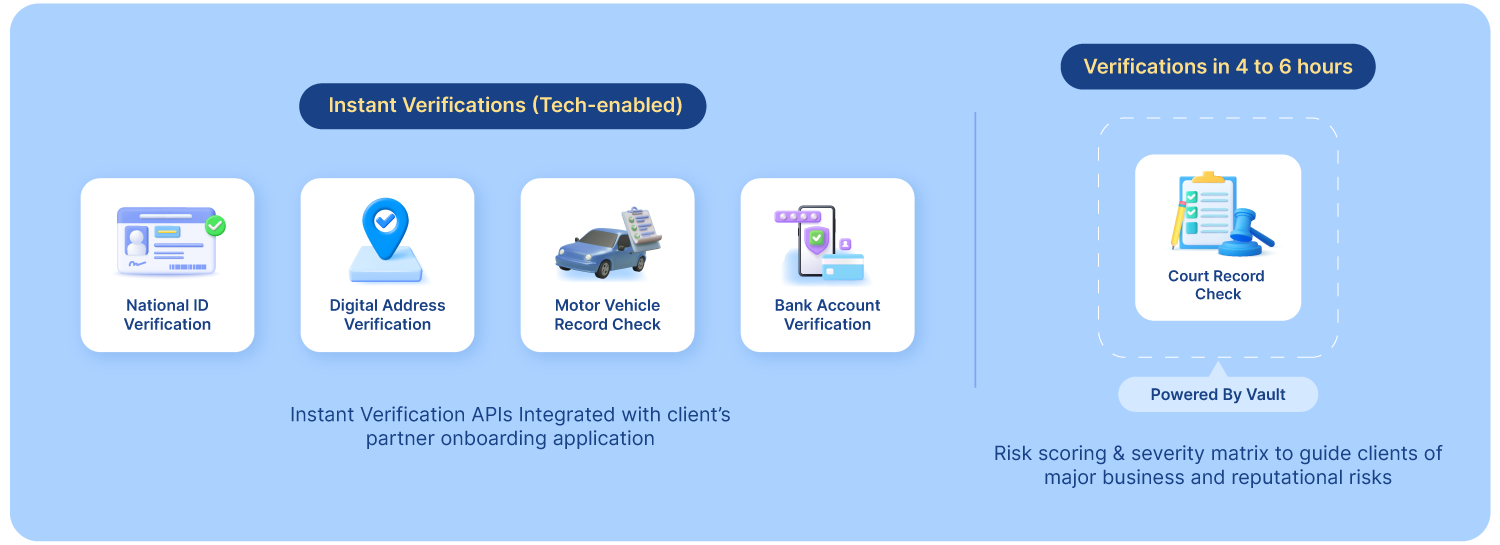

1. Digital KYC and Customer Onboarding

The BFSI sector processes numerous new accounts every month, and each account must undergo KYC (Know Your Customer) verification. Traditionally, this translated to photocopies, physical signatures, and delayed customer onboarding. RegTech transformed it into a two-minute digital process.

When a user begins onboarding, OCR (Optical Character Recognition) extracts information from Aadhaar or PAN documents, face-matching AI confirms identity in real time, and geo-fencing ensures that the interaction occurs within India’s borders. The system cross-checks data with government APIs such as CKYC, UIDAI, or GSTN.

The Reserve Bank of India’s Video-based Customer Identification Process (V-CIP) guideline, updated in 2025, has legitimised this automation. It allows fully remote onboarding while maintaining human oversight through live video interaction — one of the most successful examples of RegTech adoption globally.

2. Anti-Money-Laundering and Fraud Detection

Anti-Money-Laundering (AML) compliance requires financial institutions to monitor transactions for suspicious behaviour. This is a task that human teams alone can’t manage at scale, efficiently.

How RegTech helps in these situations:

- Behavioural analytics studies how money moves through systems like UPI, NEFT, or IMPS. If funds circulate repeatedly among linked accounts below reporting thresholds, the system flags the pattern.

- Entity resolution links multiple accounts belonging to the same individual or shell company, helping investigators see the larger network.

- Machine-learning models continuously learn from previous Suspicious Transaction Reports (STRs) submitted to the Financial Intelligence Unit (FIU-IND), improving future detection.

This approach replaces rule-based red-flagging with adaptive intelligence, significantly reducing false positives and audit fatigue.

3. Regulatory Reporting and “RegOps”

“RegOps”, short for Regulatory Operations, is the practice of automating the creation and submission of mandatory reports to regulators.

In the past, compliance officers exported data from different systems, formatted it manually, and emailed spreadsheets to RBI or SEBI. RegOps automates that entire chain.

- APIs pull data directly from core banking and trading systems.

- Validation scripts check for format accuracy and missing fields.

- RPA (Robotic Process Automation) submits the data through secure channels, creating an audit trail.

The result is near real-time reporting and fewer human errors. Regulators are also adopting SupTech (Supervisory Technology) — cloud-based portals that receive these automated submissions, allowing continuous supervision rather than quarterly reviews.

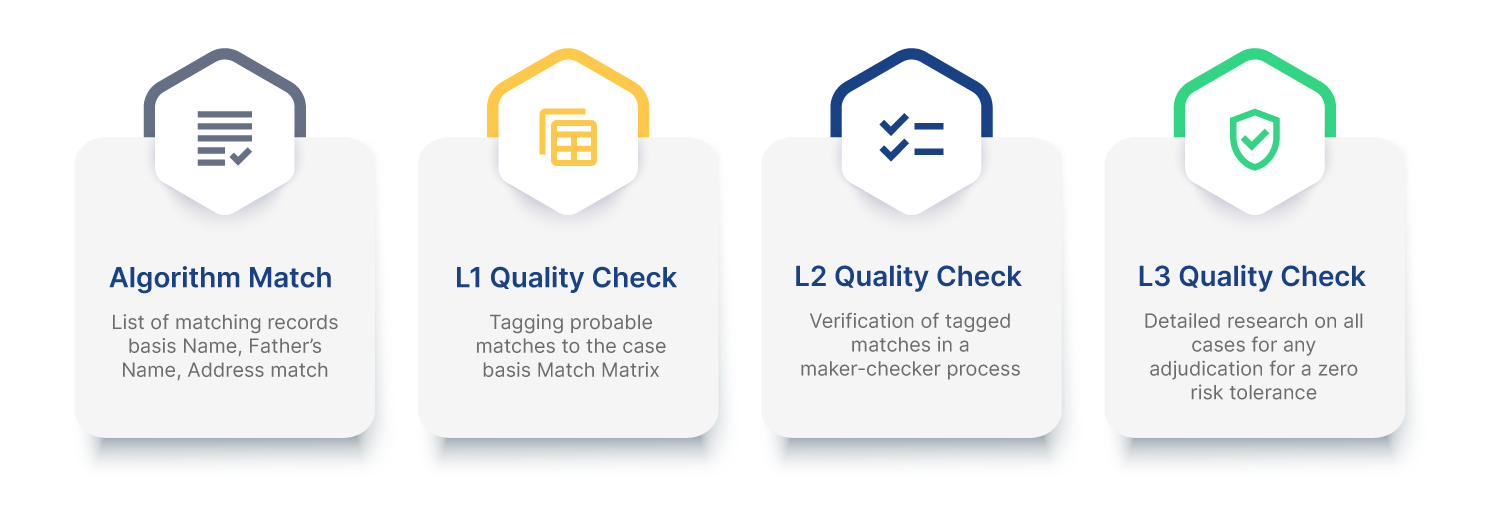

4. Corporate and Third-Party Due Diligence

As companies outsource services and build larger partner networks, knowing who you are doing business with is now extremely critical. RegTech platforms automate third-party due diligence by combining corporate registries, litigation data, financial filings, and sanctions lists into a single risk profile.

For instance:

- A bank assessing a new vendor can instantly check if the company’s directors appear on any regulatory watchlist or if their GST status is inactive.

- Some solutions even use knowledge-graph visualisation to reveal hidden ownership — such as two suppliers connected to a single black-listed promoter.

In sectors like infrastructure and renewable energy, due diligence extends to land-record verification and developer validation, ensuring that titles are clean before project finance is released.

5. Data Privacy and Consent Management

With the government asking companies to stay compliant with the changing norms and upcoming bills and acts like the DPDP Act, data privacy has now become an area of significant interest for everyone.

RegTech platforms now include privacy modules that:

- Log user consent and allow revocation at any time.

- Automate data deletion after retention periods expire.

- Generate proof of compliance during audits.

This ensures that personal data is used only for its intended purpose. For banks and insurers, it also strengthens customer confidence.

6. Risk and Governance Platforms

Many large financial institutions are replacing spreadsheet-based compliance trackers with integrated GRC (Governance, Risk, and Compliance) suites powered by RegTech. These systems map every regulation to internal policies and assign ownership within the organisation. Dashboards show real-time compliance status, overdue actions, and potential penalties.

7. Cross-Sector Adoption

While banking and NBFCs lead adoption, other sectors are catching up:

- Insurance: IRDAI-regulated insurers use RegTech to screen agents, verify policyholder identity, and detect claim fraud.

- Capital Markets: SEBI-supervised brokerages deploy trade-surveillance algorithms to detect insider trading or price manipulation.

- FinTech and Payments: Merchant-onboarding APIs check business authenticity through PAN, GST, and UDYAM verifications.

- Telecom and E-commerce: Platforms verify vendor legitimacy and monitor data privacy compliance under sectoral codes.

8. Continuous Compliance

Most companies and institutions are now racing towards continuous compliance, where checks occur automatically within business workflows rather than after the fact. A loan disbursement system, for example, won’t proceed unless KYC, PAN-GST matching, and bureau checks pass predefined thresholds, taking care of compliance before the risks emerge.

RegTech Uses Across Different Industries

Banking and Financial Services (BFSI)

The banking sector remains India’s largest RegTech user — not because it leads innovation, but because it faces the highest regulatory exposure. Every loan disbursal, fund transfer, or deposit activity sits under the RBI’s compliance framework.

To manage this volume, banks have adopted automated AML systems, real-time transaction-monitoring dashboards, and AI-driven risk-classification tools. The impact? What once took days and weeks of manual reconciliation is now handled in near real time. This translates to reduced compliance costs, faster reporting cycles, and little to no regulatory breaches.

FinTech and Digital Payments

FinTechs built their reputation on speed and simplicity — but that speed must coexist with accountability. RegTech ensures that growth doesn’t come at the cost of governance and compliance issues.

Payment aggregators and digital lenders now embed e-KYC APIs, sanction-screening checks, and consent-management systems directly into their platforms.

As UPI and wallet transactions continue to multiply, behaviour analytics engines monitor micro-payments for suspicious clustering, while RPA scripts prepare statutory reports automatically.

Insurance

Insurance companies face two significant hurdles: abiding by the regulations from IRDAI and the complex operations of verifying customers, intermediaries, and claims.

RegTech solutions help insurers verify agent credentials, policyholder identity, and claim authenticity in real time. OCR and facial-matching systems validate documents instantly, and anomaly-detection models flag duplicate or inflated claims.

With DPDP rules now binding insurers to safeguard sensitive health and financial data, including Personally Identifiable Information (PII), RegTech tools also handle consent logging, encryption auditing, and retention-period monitoring.

Capital Markets

The capital markets ecosystem, consisting of brokers, depositories, fund houses, and exchanges, uses RegTech to keep trading transparent and compliant with various regulatory guidelines.

Machine-learning systems analyse millions of orders to detect patterns such as circular trading, insider transactions, or collusive behaviour. Trade-surveillance tools also cross-reference market data with communication logs and timing patterns, producing alerts within seconds rather than days.

Fund houses employ automated compliance dashboards to track investment limits, related-party transactions, and exposure thresholds. The net effect is a market that can self-monitor almost as quickly as it trades.

Corporate and Enterprise Sector

Procurement and compliance teams in companies use integrated platforms to assess vendor legitimacy, cross-verify director identities through MCA filings, track litigation exposure, and monitor credit signals. For manufacturers, logistics providers, and infrastructure developers, this prevents reputational risk from non-compliant partners.

In real-estate-linked sectors, land-record verification and ownership checks are now standard before financing or acquisitions. Continuous monitoring ensures that any change in ownership, insolvency status, or regulatory flag triggers an instant alert.

Regulators and Supervisory Bodies

Regulators themselves are becoming part of the RegTech ecosystem through Supervisory Technology (SupTech). RBI and SEBI are piloting frameworks where banks and intermediaries submit structured data via APIs rather than static reports.

This allows supervisors to track compliance indicators continuously, identify systemic risks earlier, and reduce manual interpretation errors. For the first time, both the regulator and the regulated are operating on a shared digital backbone — improving transparency and mutual trust.

Differences Between FinTech and RegTech

FinTech and RegTech are two terms that you will find used often, interchangeably. However, they are not the same thing. FinTech, which reimagines how money moves, and RegTech, which ensures that those movements remain compliant and secure.

Both rely on data, automation, and APIs, yet their intent and impact differ heavily.

What Is FinTech?

FinTech — short for financial technology — transformed finance from a slow, paper-driven process into a click-based service. In India, it turned payments into tap-to-pay experiences and lending into instant approvals. From UPI and neobanks to BNPL and digital investment apps, FinTech built the rails that now carry billions of daily transactions.

The sector’s purpose is inclusion and efficiency: bringing formal financial services to every smartphone user. But that very scale creates vulnerabilities.

Every new API call, every customer onboarding, and every stored dataset introduces regulatory exposure — around data protection, anti-money-laundering (AML), and KYC compliance.

This need for constant, automated oversight gave rise to RegTech.

FinTech vs RegTech — Key Differences

Aspect | FinTech | RegTech |

Core Purpose | Expand access and convenience | Ensure compliance, accuracy |

Primary Users | Consumers, lenders, merchants | Banks, regulators, compliance teams |

Focus Area | Payments, credit, wealth | KYC, AML, reporting |

Measure of Success | Adoption and revenue | Trust and risk reduction |

How RegTech Complements FinTech

In practice, the two work in tandem.

- A lending app relies on RegTech APIs to verify PAN, Aadhaar, and CKYC data instantly.

- A payments platform uses transaction-monitoring engines to flag suspicious behaviour.

- An insurance portal automates claim checks and records every consent trail.

FinTech drives customer interaction; RegTech ensures regulatory integrity. Together, they make financial inclusion sustainable rather than experimental.

AuthBridge As Your RegTech Partner

Indian regulators have moved from periodic oversight to continuous supervision, with many of the regulators now requiring evidence of continuous compliance. Here’s why AuthBridge remains one of the top RegTech platforms in India today:

1. Automating RBI KYC and PMLA Obligations for the BFSI Sector

- Identity APIs linking PAN, Aadhaar (offline XML/QR modes), CKYC, Voter ID, and Udyam registries.

- AML Screening against RBI, SEBI, FIU-India, and global watchlists.

- Geo-verified Video KYC using face-match, liveness, and timestamped audit logs to satisfy RBI’s V-CIP norms.

- Regulatory Reporting Feeds are exportable in machine-readable formats for RBI inspection tools like DAKSH.

This replaces paper-based KYC and spreadsheet tracking with verifiable digital records that meet both RBI and FIU expectations.

2. Fraud Prevention and Agent Verification

- Agent Licence Verification is directly mapped to the IRDAI registries.

- OCR and Document AI to extract and validate policy and claim data.

- Facial Recognition and Duplicate-Claim Detection to flag fraud patterns.

- Consent and Data Handling Workflows aligned to DPDP privacy principles.

Insurers can establish audit trails for every agent and claim interaction without manual reconciliation.

3. Capital Markets

- Corporate KYB & UBO Mapping via MCA and GSTN data to identify direct and indirect owners.

- Litigation and Adverse-Media Screening using NLP to detect disclosure risks.

Brokerages and fund houses use these feeds to maintain “always-clean” UBO records for SEBI reporting.

4. Third-Party Due Diligence and ESG Readiness

- Vendor and Distributor Verification through MCA, GST, and Udyam registries.

- Litigation & Insolvency Tracking via NCLT and court databases.

- Land and Asset Ownership Verification for project finance and lease compliance.

- Periodic Re-verification triggers when ownership or registration changes.

This gives manufacturers and developers evidence-based supply-chain integrity for ESG and anti-bribery audits.

5. Data Protection and Consent in line with DPDP Act

- Consent Ledger: Cryptographically sealed consent artefacts linked to every verification.

- Role-Based Access and Data Residency Controls: ensuring processing within India.

- Retention and Deletion Automation: for DPDP Schedule compliance.

Organisations can produce proof of lawful processing and user consent on demand.

6. Technology Stack and Delivery Assurance

- Secure API Gateway with JWT/OAuth authentication and transaction-level logging.

- AI/ML Models for OCR, face comparison, liveness detection, and document classification.

- NLP Pipelines for court data and adverse-media analysis.

- India-hosted cloud infrastructure for regulatory data residency.

Across BFSI and enterprise sectors, AuthBridge’s RegTech infrastructure allows compliance teams to generate machine-readable evidence aligned with RBI, SEBI, IRDAI, and DPDP requirements. It transforms oversight into operational governance, where every KYC, KYB, and consent record is instantly provable.