Digital KYC Solution for Identity Verification

Our image-based Digital KYC enables end-to-end seamless customer onboarding journeys through AI-powered facial recognition, liveness detection, OCR, and geo-tagging technologies, adding speed and scale to your customer onboarding process

Trusted by 2,000+ companies

Intelligent KYC solutions to digitize your onboarding and authentication processes

Truly Digital Solution in Every Sense

Realtime Identity Verification

Selfie backed Liveness Check, Face Match Score against NIDs and

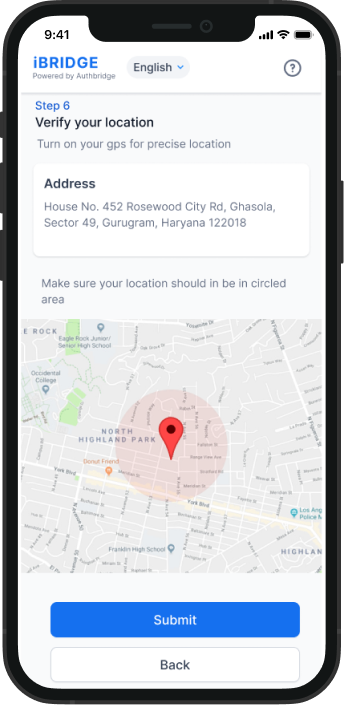

Geo-coding based digital address verification

Hassle Free

Integrations

Integrable with LOS/LMS/CRMS

via API and SDK based integrations

with API documentation and developer support

Secure and Compliant Processes

Take and manage customer Consent with ease and Mask Sensitive customer data with an ISO 27001 compliant solution

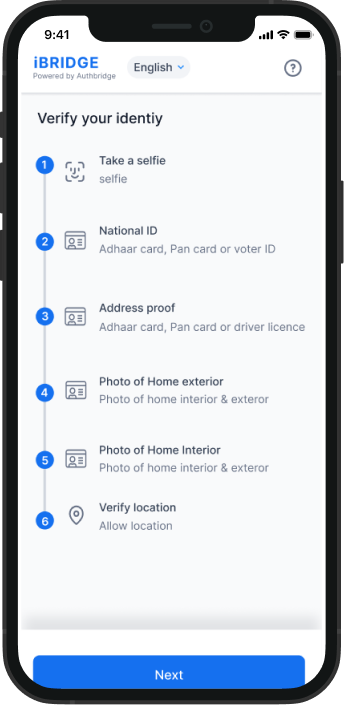

Process of Digital KYC Verification

AuthBridge's Digital KYC Solution

Give your Customers a Seamless Onboarding and Verification Experience

Step 1

Mobile Number Verification with OTP and consent based verification

Step 2

Capture Selfie for Liveness Check and get a match score

Step 3

OCR enabled POI/POA Verification to auto extract Identity and address details

Step 4

Successful Customer Identification and KYC acceptance/rejection

AI to make Digital KYC contactless

Leverage the power of artificial intelligence and machine learning to create real-time, contactless onboarding journeys. Enhance your customer experience and scale up faster with our KYC Solutions.

Cost Optimization

Reduced costs, customizable workflows, compliant process

Our Digital KYC product enables instant verification with the power of AI, ML, and deep search algorithms ensuring the fastest onboarding process for your customers, reduced operational costs, helping your organisation scale up at speed. Our Digital KYC comes with customizable workflows so you can create your industry-specific KYC journeys. Our Digital KYC product is data-security compliant and ensures complete adherence to the latest RBI guidelines.

Security Compliant

SEBI, RBI Adherence

Data

Privacy

Fewer KYC Dropouts

Reduced customer application dropout rates with Digital KYC

Traditional KYC involved cumbersome paperwork that led to higher drop-out rates in customer onboarding. Our Digital KYC solution makes the process completely digital, eliminating paperwork completely, making the whole journey contactless, enhancing your customer experience, thus reducing your customer drop-out rates significantly.

Minimal Drop Outs

Contactless KYC

No Paper Work

No More Identity Frauds

Accurate face match percentage, liveness detection to catch identity frauds

Our AI-powered image recognition and liveness detection technologies use biometric anti-spoof algorithms to test the genuineness of the image taken and matches it with valid ID proof, ensuring that an entity is who they say they are. Get notified each time there is a skewed, blurry or disoriented image right at the beginning of the onboarding process so that you can catch discrepancies and potential identity thefts with AI-powered high-quality image processing

Face Match Check

Name Match Check

Address Match

Remote Onboarding

Easily Onboard customers from remote locations

Digital KYC has a higher scope and much better customer reach because the entire process is contactless. This means anyone with Aadhar card and the registered mobile number can perform our Digital KYC remotely. This is especially helpful in achieving a wider customer reach in rural areas where access to banks and financial institutions is relatively lower than in urban areas. , It helps you save operational costs by up to 70% and onboarding time by up to 90%. Banks, NBFCs, mutual funds, insurance, logistics, telecom companies, mobile wallets, and P2P marketplaces can use Digital KYC for seamless customer onboarding journeys.

Mobile Verification

Aadhaar Verification

Pan India Support

Top Instant Verification APIs used by our Clients for KYC services

Instant verification and onboarding with API based KYC services

Aadhaar Card Verification API

PAN Card Verification API

Voter Card Verification API

Passport Verification API

Driving License Verification API

Bank Account Verification API

RC VerificationAPI

Face Verification API

Powering KYC Technologies for 30+ Industries

KYC Solution for All Industries

Banking and Financial Services

Onboard and verify customers, borrowers and users

Real Money Gaming

Faster authentication of players to accelerate onboarding

Jewellery

Verify the buyers to prevent identity theft and money laundering

Internet/E-commerce

Verify the users and sellers to prevent frauds

Insurance

Authenticate the policy holders to ensure credibility

Healthcare & Pharma

Verify the medical reps, doctors and other medical staff

Telecommunication

Fastrack onboarding and verification of new users

Rental/Real Estate

Verification and registration of tenants

Expert insights at your finger tips.

All things Background verification, Due Diligence , candidate experience and more.

Blog

Digital KYC: Transforming The BFSI Industry

The BFSI industry, which includes banking, financial services, and insurance, is undergoing a radical change as a result of the modern world’s…

Read more >>

Newsroom

Importance of Background Verification in BFSI Sector

The point of an exponential boom in any industry is crucial for two reasons. Expectedly, it opens the industry and stakeholders to unprecedented..

Read more >>

Blog

KYC – How Does KYC Complement Identity Verification?

While it is important for businesses to know their employees, it is equally important that they know their customers and/or clients. That is why KYC…

Read more >>

Contact Sales

Ready to Explore AuthBridge for your business?

We’d love to show you how AuthBridge can help your business. Fill out the form and we’ll be in touch within 24 hours.

- Assess your team’s needs

- Learn more about AuthBridge Product & features

- Discuss pricing options

By submitting this form you are agreeing to our privacy policy.

Digital KYC: A Comprehensive Guide

This article will explain what Digital KYC is. Image-based Digital KYC for end-to-end customer onboarding with AI-powered facial recognition, liveliness detection, OCR & geo-tagging technologies.

Table of Contents

Click a topic to scroll directly to it.

Digital KYC Definition

Digital KYC (Know Your Customer) is an electronic process for verifying the identity of customers, primarily used by financial institutions to ensure compliance with regulatory requirements. This process involves collecting and verifying customer information through digital means, thereby facilitating faster and more efficient customer onboarding.

Evolution of KYC Practices

Traditional KYC methods involved manual verification of documents, which was time-consuming and prone to errors. The advent of digital KYC has revolutionized this process by leveraging technology to automate identity verification, thereby reducing the time and cost associated with KYC compliance. The shift towards digital KYC has been driven by advancements in technology, regulatory changes, and the need for improved customer experiences.

According to a report by MarketsandMarkets, the global digital identity solutions market is expected to grow from USD 13.7 billion in 2021 to USD 30.5 billion by 2026, at a CAGR of 17.3%. This growth underscores the increasing adoption of digital KYC solutions across various industries.

Try Fast, Accurate, & 100% Digital Checks Now

Digital KYC Regulatory Framework

1. Global Standards and FATF Guidelines

The Financial Action Task Force (FATF) sets international standards for combating money laundering and terrorist financing. These guidelines are instrumental in shaping digital KYC practices globally. FATF recommends a risk-based approach to customer due diligence, which has been adopted by many countries to enhance the effectiveness of their KYC processes.

2. Indian Legal Framework: PMLA, 2002 and RBI Directions

In India, the Prevention of Money Laundering Act (PMLA), 2002, provides the legal basis for KYC regulations. The Reserve Bank of India (RBI) has issued detailed guidelines to regulated entities, mandating the use of digital KYC for customer verification. Key highlights include the use of Aadhaar for eKYC verification and the implementation of the Video-Based Customer Identification Process (V-CIP).

Components of Digital KYC

1. Customer Identification Procedure (CIP)

The Customer Identification Procedure (CIP) is the foundational step in the digital KYC process. It involves collecting basic information such as the customer’s name, address, date of birth, and identification number. This information is then verified against official documents to ensure accuracy and authenticity.

2. Customer Due Diligence (CDD)

Customer Due Diligence (CDD) involves a deeper assessment of the customer’s background to prevent money laundering and terrorist financing. CDD can be categorised into two types:

Enhanced Due Diligence (EDD): Applied to high-risk customers, requiring additional verification and scrutiny.

Simplified Due Diligence (SDD): Used for low-risk customers, involving a more straightforward verification process.

3. Beneficial Ownership Identification

This component ensures that the true beneficial owners of an account or entity are identified. It is particularly crucial for corporate accounts and helps in preventing the concealment of illicit funds.

Try Fast, Accurate, & 100% Digital Checks Now

Implementation and Compliance

1. Requirements for Regulated Entities

Regulated entities, such as banks and financial institutions, are required to implement digital KYC processes in compliance with regulatory standards. These requirements include maintaining updated customer records, conducting regular audits, and ensuring that KYC processes are in line with legal frameworks.

2. Documentation and Record Management

Effective documentation and record management are crucial for compliance. Regulated entities must store customer information securely, ensuring data privacy and integrity. Digital KYC solutions often include cloud-based storage options that provide scalable and secure record-keeping.

3. Reporting Obligations to FIU-India

Financial institutions in India must report suspicious transactions and maintain records of customer identification data as per the guidelines set by the Financial Intelligence Unit (FIU-India). This reporting is essential for monitoring and preventing money laundering and other financial crimes.

Benefits of Digital KYC

1. Efficiency and Speed

Digital KYC significantly reduces the time required for customer verification, enabling faster onboarding processes. Automated systems can verify documents and customer information within minutes, compared to the days or even weeks required for manual verification. This efficiency not only improves operational workflows but also enhances overall productivity.

2. Improved Customer Experience

By offering a seamless and convenient onboarding experience, digital KYC enhances customer satisfaction. Customers can complete the verification process remotely, without the need to visit physical branches or submit paper documents. This convenience is particularly beneficial in the fintech and banking sectors, where quick and efficient service is paramount.

3. Enhanced Security and Fraud Prevention

Digital KYC employs advanced technologies such as AI and biometrics to verify customer identities accurately. These technologies help detect fraudulent activities by cross-referencing data from multiple sources and identifying inconsistencies. As a result, digital KYC provides a more secure verification process, protecting both institutions and customers from potential fraud.

A study by McKinsey & Company found that digital KYC can reduce customer onboarding time by up to 90%, while also cutting costs by 70%. These figures illustrate the substantial benefits that digital KYC offers in terms of efficiency and cost savings.

Challenges and Solutions with Digital KYC

1. Data Privacy and Security Concerns

One of the primary challenges in digital KYC is ensuring data privacy and security. The collection and storage of sensitive customer information necessitate robust security measures to prevent data breaches and unauthorised access. Institutions must comply with data protection regulations like GDPR and India’s Data Protection Bill to safeguard customer data.

2. Technological and Operational Challenges

Implementing digital KYC solutions involves integrating new technologies into existing systems, which can be complex and costly. Additionally, institutions must ensure that their staff are adequately trained to use these technologies effectively. Interoperability between different systems and maintaining the accuracy of automated processes are also critical challenges.

3. Solutions

Advanced Encryption: Utilising strong encryption methods to protect data during transmission and storage.

Regular Audits: Conducting frequent security audits to identify and mitigate vulnerabilities.

Staff Training: Ensuring that employees are trained in using digital KYC systems and understanding compliance requirements.

4. Interoperable Systems: Developing systems that can seamlessly integrate with existing infrastructure to ensure smooth operations.

AuthBridge’s Digital KYC Solution

AuthBridge’s Digital KYC solution offers a comprehensive, seamless, and secure process for customer onboarding and identity verification, leveraging advanced technologies like AI, ML, OCR, and biometric verification. Here’s a detailed look at the process and features:

1. Mobile Number Verification

The process begins with verifying the customer’s mobile number using an OTP-based system, ensuring consent and initial validation.

2. Selfie Capture and Liveness Check

Customers capture a selfie, which is used for a liveness check. This step ensures that the person is physically present and not using a photograph or video. The captured image is compared against national ID databases to calculate a face match score.

3. Document Verification

AuthBridge uses OCR-enabled technology to verify Proof of Identity (POI) and Proof of Address (POA) documents. This software automatically extracts necessary details, such as name and address, from the documents.

4. Customer Identification and Decision

Based on the data collected and verified, the system decides on KYC acceptance or rejection, completing the verification process.

Solutions and Technologies

- AI-Powered KYC: Utilises artificial intelligence to enhance the accuracy and efficiency of the verification process.

- Biometric Verification: Incorporates fingerprint and facial recognition technologies to authenticate identities.

- OCR Technology: Automates the extraction and verification of document details, reducing manual errors.

- Geo-Tagging: Ensures the geographical location of the customer matches the provided address, enhancing security.

Benefits

- Efficiency and Speed: The digital process significantly reduces the time required for KYC, enabling instant verification and faster customer onboarding.

- Cost Reduction: By automating the KYC process, operational costs are reduced, and manual efforts are minimised.

- Compliance: Ensures adherence to regulatory guidelines, including SEBI and RBI standards, ensuring a secure and compliant verification process.

- Security: Advanced encryption and security protocols protect customer data, ensuring privacy and preventing frauds.