Get Personalised Solutions As Per Your Requirements

Connect with our sales team and get solutions to all your queries, alongside custom solutions for your needs.

GST Rates In India: Comprehensive Guide

Abhinandan Banerjee • February 5, 2026

The Goods and Services Tax (GST) was introduced in India on July 1, 2017, marking a significant reform in the country's indirect tax system. Its primary objective was to consolidate multiple taxes into a single tax, aiming to eliminate tax-on-tax (cascading effect), simplify the tax structure, and make goods and services more affordable for consumers. The GST system sought to enhance the ease of doing business by creating a unified national market.

Key Features of the GST Framework

GST is characterized by its multi-tiered structure, with rates ranging from 0% to 28%, depending on the goods or services. It encompasses all Indian states, bringing them under a common tax regime and facilitating seamless interstate commerce. The framework operates on a dual model, where both the Central and State governments levy taxes on goods and services, ensuring revenue sharing between them.

Benefits of GST: Catalyzing Economic Transformation

Creating a Unified Tax System

One of the most significant benefits of GST is the creation of a unified tax system, which has replaced a complex web of central and state taxes. This unification has not only simplified the tax landscape but also reduced compliance burdens on businesses, promoting a more conducive environment for growth and expansion.

Mitigating the Cascading Effect of Taxes

By allowing the set-off of prior-stage taxes, GST has effectively reduced the cascading effect that was prevalent in the previous tax regime. This means that the tax is only paid on the value addition at each stage of the supply chain, making goods and services cheaper for the end consumer.

Enhancing Compliance and Widening the Tax Base

The GST framework, supported by a comprehensive IT system (GSTN), has improved tax compliance by making the process more straightforward and transparent. This, coupled with measures such as the e-way bill, has widened the tax base, bringing more businesses into the formal economy.

The Impact of GST on Various Sectors

Boost to the Manufacturing Sector

GST has significantly benefited the manufacturing sector by reducing the cost of production. The seamless flow of input tax credits across state boundaries has encouraged manufacturers to optimize their supply chains, leading to increased efficiency and competitiveness.

Implications for the Service Industry

The service industry has seen a simplification in tax procedures under GST, with a uniform rate being applied across the country. This has eliminated the confusion around service tax rates and compliance requirements that varied by state under the previous regime.

Effects on the Consumer Goods Sector

Consumers have benefited from GST through the elimination of the cascading effect of taxes, which has led to a reduction in the overall tax burden on goods. While the impact varies across product categories, the overall trend has been positive, with many consumer goods becoming more affordable.

The Multi-Tiered GST Rate Structure

The GST Council, a federal body overseeing GST implementation, determines the tax rates for various goods and services. Currently, India follows a five-tiered GST rate structure, categorized by the percentage of tax levied:

GST Rate Structure in India

GST Rate (%) | Description | Examples |

0 (Nil Rated) | Essential goods and services considered vital for basic needs | Fresh fruits & vegetables, Milk, Bread, Unbranded cereals, Newspapers |

5% | Essential items and commonly consumed goods | Processed foods (milk powder, pulses), Footwear below Rs. 1000, Textiles |

12% | A wide range of goods and services considered necessities or comforts | Processed food items (biscuits, chocolates), Non-AC restaurants, Mobile phones, Commercial accommodation (below Rs. 1000 per day) |

18% | Most consumer durables and some luxury items | Televisions, Refrigerators, Washing machines, Beauty products |

28% | Luxury items and demerit goods | Jewelry, Air conditioners, Automobiles, Tobacco products |

Source: Central Board of Indirect Taxes and Customs (CBIC) website -https://cbic-gst.gov.in/

Key Points to Consider:

- The 0% (Nil Rated) slab exempts essential commodities from GST, ensuring affordability for basic needs.

- The 5% slab provides a lower tax burden on commonly consumed goods.

- The 12% and 18% slabs encompass a broad spectrum of goods and services, catering to various necessities and comforts.

- The 28% slab applies to luxury items and demerit goods (like tobacco) to discourage excessive consumption and generate higher tax revenue.

Understanding HSN Codes and Schedule of GST Rates:

The CBIC website offers a comprehensive "Schedule of GST Rates" document that classifies goods and services based on their Harmonized System of Nomenclature (HSN) code. This internationally standardized system plays a crucial role in identifying and classifying goods for customs and tax purposes.

By referring to this document, businesses and individuals can determine the specific GST rate applicable to their product or service based on its HSN code. You can access the document by following these steps:

- Visit the CBIC website: https://cbic-gst.gov.in/

- Navigate to the "Notifications" section.

- Under "Central Tax (Rate)" notifications, locate the latest notification regarding Schedule of GST Rates (e.g., Notification No. 01/2024-Central Tax (Rate) dated June 30, 2023).

- Download the notification document.

Importance of Staying Updated on GST Rates:

The GST Council periodically reviews and revises tax rates. Businesses and individuals must stay informed about these changes to ensure accurate tax compliance. Regularly checking the CBIC website and consulting with tax professionals are essential practices.

Statistics on GST Revenue and Rate Rationalization:

Since its implementation, GST has significantly improved tax collection efficiency in India. Here are some key statistics highlighting its impact:

- As of March 2023, India's monthly average GST collection has surpassed Rs. 1.4 lakh crore. (Source: Ministry of Finance, PIB India)

- The government aims to achieve further simplification and rationalization of GST rates in the future. Potential areas of focus include merging certain slabs and streamlining exemptions. (Source: Industry reports and news articles on GST reforms)

GST Rate Structure Breakdown and Rationale

0% (Nil Rated):

- Description: This slab exempts essential goods and services considered vital for basic needs.

- Examples: Fresh fruits & vegetables, Milk, Bread, Unbranded cereals, Newspapers.

- Rationale: Exempting these necessities ensures affordability for a broader population segment and promotes social welfare.

5%:

- Description: This category applies a lower tax rate to commonly consumed goods.

- Examples: Processed foods (milk powder, pulses), Footwear below Rs. 1000, Textiles.

- Rationale: The lower tax burden keeps these essential items affordable while enabling the government to generate some revenue.

12%:

- Description: This broad slab encompasses a wide range of goods and services considered necessities or comforts.

- Examples: Processed food items (biscuits, chocolates), Non-AC restaurants, Mobile phones, Commercial accommodation (below Rs. 1000 per day).

- Rationale: This standard rate applies to a significant portion of economic activity, balancing revenue generation with consumer affordability.

18%:

- Description: This slab applies to most consumer durables and some luxury items.

- Examples: Televisions, Refrigerators, Washing machines, Beauty products.

- Rationale: The higher tax rate discourages excessive consumption of non-essential goods and generates additional tax revenue.

28%:

- Description: This highest slab applies to luxury items and demerit goods (like tobacco) to discourage excessive consumption.

- Examples: Jewelry, Air conditioners, Automobiles, Tobacco products.

- Rationale: The significant tax burden aims to limit consumption of luxury goods and generate substantial tax revenue to support government initiatives.

Overview of SGST, CGST, and IGST

At the heart of the GST system are three primary components: the State Goods and Services Tax (SGST), the Central Goods and Services Tax (CGST), and the Integrated Goods and Services Tax (IGST). Each serves a distinct role in the taxation structure, catering to state, central, and interstate transactions, respectively.

SGST: State Goods and Services Tax

Role and Applicability of SGST

SGST is levied by individual state governments on intra-state transactions of goods and services. It represents the state’s share of the GST revenue from transactions occurring within its territory, ensuring that states retain their fiscal autonomy and revenue streams in the GST era.

Impact on State Revenue and Autonomy

The introduction of SGST has been pivotal in maintaining the fiscal balance between the central and state governments. By securing a steady revenue stream for states, SGST supports local infrastructure development, welfare schemes, and other state-specific projects.

CGST: Central Goods and Services Tax

Role and Applicability of CGST

CGST is imposed by the central government on intra-state transactions, collected alongside SGST. It embodies the central government's portion of GST revenue from transactions within a state, ensuring a uniform tax structure across the country.

Central Government’s Revenue Mechanism

CGST has streamlined the central government’s taxation mechanism, reducing complexity and ensuring a consistent revenue flow from across the states. This uniformity aids in national-level infrastructure projects and central welfare initiatives.

IGST: Integrated Goods and Services Tax

Role and Applicability of IGST

IGST is charged on all interstate transactions of goods and services, as well as imports. Administered by the central government, IGST ensures that tax is collected in the state where the goods or services are consumed, adhering to the destination principle.

Facilitating Interstate Trade and Commerce

IGST has been instrumental in simplifying tax on interstate commerce, eliminating the need for separate state taxes that hindered the free flow of goods across state borders. This has significantly boosted interstate trade and facilitated a more integrated national market.

Comparative Analysis: SGST, CGST, and IGST

Distinctions in Tax Collection and Distribution

While SGST and CGST are levied concurrently on intra-state transactions, IGST uniquely caters to interstate transactions. The revenue collected under IGST is shared between the originating and destination states, according to pre-defined distribution criteria, ensuring equitable revenue sharing.

Examples of Tax Application in Different Scenarios

For instance, a product manufactured in State A and sold within the same state will attract SGST and CGST. However, if the same product is sold to State B, it will attract IGST, which will be shared between State A and State B.

Strategic Implications for Businesses and Consumers

Navigating Compliance with SGST, CGST, and IGST

Businesses must adeptly navigate the GST framework to ensure compliance, optimize tax credits, and minimize liabilities. Understanding the applicability and procedural nuances of SGST, CGST, and IGST is crucial for accurate tax filing and planning.

Tax Planning and Optimization Strategies

Effective tax planning strategies involve leveraging the input tax credit system across SGST, CGST, and IGST to optimize tax payments. Businesses can significantly reduce their tax burden by understanding and utilizing the interplay between these taxes efficiently.

Identifying GST Rates for Products and Services

Official GST Rate Finder Tools

Official GST Portal and Mobile Apps: The government has provided official tools such as the GST portal (https://www.gst.gov.in/) and the GST Rate Finder mobile app to help individuals and businesses find applicable GST rates. These platforms are regularly updated and offer a search function where users can input the name or HSN code (Harmonized System of Nomenclature) of a product or the SAC code (Services Accounting Code) for services to find the corresponding GST rate.

Understanding HSN and SAC Codes

HSN Codes for Goods: The HSN system is a globally standardized system of names and numbers to classify traded products. In India, businesses with a turnover of more than 1.5 crores INR are required to use a 4-digit HSN code, while those with a turnover of more than 5 crores INR use a 6-digit code.

SAC Codes for Services: Similar to HSN codes for goods, services are classified under SAC codes. These codes are used to identify the GST rates applicable to various services.

Consulting with Tax Experts

Role of Tax Consultants: For businesses and individuals unsure about the applicable GST rates for their products or services, consulting with a tax expert or a GST practitioner can be beneficial. These professionals can provide personalized advice, taking into account the latest GST notifications and amendments.

Utilizing Online GST Calculators

Online Tools for Quick Calculations: Various financial websites and tax advisory platforms offer online GST calculators. These tools allow users to calculate the GST on a product or service by inputting the base price and selecting the applicable GST rate. While convenient for quick estimates, users should ensure they are using updated rates for accurate calculations.

Navigating GST Rate Changes and Updates

Understanding the Process of GST Rate Revision

The GST Council, the apex decision-making body concerning the Goods and Services Tax in India, meets regularly to review and revise GST rates. These changes are made based on industry feedback, economic data, and the need to stimulate growth or regulate consumption of certain goods and services. Keeping abreast of these updates is crucial for businesses and consumers to ensure compliance and make informed financial decisions.

Official Notifications and Circulars

Staying Updated with Official Sources: The Central Board of Indirect Taxes and Customs (CBIC) and the GST Council release notifications, circulars, and press releases to announce changes in GST rates. Businesses should regularly check these official sources or subscribe to updates to stay informed about any changes that may affect their products or services.

Impact of GST Rate Changes on Pricing Strategies

Adjusting Business Pricing: Any change in GST rates can significantly impact a business's pricing strategy. For instance, a decrease in the GST rate provides an opportunity to reduce the price, potentially increasing demand. Conversely, an increase in GST rates may require businesses to absorb the additional cost or pass it on to consumers, affecting sales and profit margins.

Accounting Software and GST Compliance

Automating GST Rate Updates: Modern accounting and billing software come equipped with features to automatically update GST rates as per the latest notifications. This automation helps businesses remain compliant without manual intervention, ensuring that invoices reflect the correct GST rates. Selecting software that offers seamless updates and compliance features is essential for efficient business operations.

Preparing for GST Audits and Compliance Checks

Ensuring Compliance: With the dynamic nature of GST rates, businesses must maintain accurate records and invoices that reflect the correct rates. Regular internal audits and compliance checks can help identify and rectify discrepancies, preparing businesses for potential GST audits by authorities. Utilizing GST compliance tools and software can streamline this process, reducing the risk of non-compliance penalties.

Leveraging Technology for GST Compliance and Rate Discovery

Embracing Digital Solutions in the GST Regime

The advent of GST has ushered in a new era of digital compliance, with technology playing a pivotal role in how businesses manage their taxes. Leveraging technology not only simplifies the process of determining applicable GST rates but also ensures accuracy and efficiency in filing returns, claiming input tax credits, and maintaining compliance with GST regulations.

GST Compliance Software

Features and Benefits: GST compliance software solutions offer a range of features designed to automate and streamline tax-related processes. These include auto-calculating GST rates for invoices, generating GST returns, and keeping track of changes in GST laws. By choosing a software solution that integrates with existing business systems (like ERP or accounting software), businesses can ensure a seamless flow of financial data, minimizing errors and saving time.

AI and Machine Learning in GST Rate Determination

Innovative Approaches to GST Compliance: The application of AI and machine learning technologies is revolutionizing how businesses approach GST rate determination and compliance. These technologies can analyze vast amounts of data to identify the correct GST rates for products or services, predict GST liabilities, and even suggest optimizations for tax credits. As these technologies evolve, they promise to offer more sophisticated solutions to GST compliance challenges.

Mobile Applications for On-the-Go GST Management

GST Rate Finder and Compliance Apps: Numerous mobile applications are available that enable businesses and individuals to find GST rates, calculate GST amounts, and even file GST returns directly from their smartphones. These apps are particularly useful for small and medium-sized enterprises (SMEs) and individual professionals who need a flexible and accessible solution for managing GST obligations on the go.

Exempt Goods and Services under GST in India (As of March 29, 2024)

The Goods and Services Tax (GST) system in India exempts certain categories of goods and services from levy. This exemption aims to ensure affordability of essential items, promote specific sectors, and streamline tax administration. Here's a comprehensive list of exempt goods and services under GST, incorporating data from official government sources:

Source: Central Board of Indirect Taxes and Customs (CBIC) website -https://cbic-gst.gov.in/

Exempt Goods:

- Agricultural Produce: Fresh fruits, vegetables, food grains (wheat, rice, cereals), pulses, unprocessed spices, flowers, leaves, seeds, and fodder. (Schedule 1 of the CGST Act)

- Livestock: Live animals (excluding horses meant for racing) including poultry, fish, worms, silk cocoons, and their eggs.

- Certain Food Items: Milk, curd, lassi, buttermilk, cheese (excluding processed cheese), honey, jaggery, and agricultural implements.

- Essential Supplies: Salt, unbranded cereals, and educational supplies like maps, globes, and charts.

- Textiles: Certain handloom fabrics, khadi (cotton fabric used for traditional Indian clothing), and fibers like raw jute and silk waste.

- Natural Resources: Uncut and unpolished diamonds, and natural gas for domestic consumption.

Exempt Services:

- Healthcare: Services provided by a clinical establishment, except for those with room charges exceeding Rs. 5000 per day.

- Education: Services provided by educational institutions by way of teaching. (Excludes coaching and entrance exam related services)

- Financial Services: Certain financial services like long-term insurance, life insurance, and banking services.

- Religious and Charitable Services: Services provided by religious institutions and charitable activities for public welfare.

- Public Transport: Services related to transportation of passengers by public transport vehicles like railways, buses, and metros.

- Funeral Services: Services related to burials and cremations.

Additional Exempt Categories:

- Supply of Goods from a Non-Taxable Territory: Goods supplied from a non-taxable territory (like Jammu & Kashmir) to another non-taxable territory without entering India are exempt.

- Exports: Export of goods and services out of India is generally exempt under GST. (Zero-rated supply)

Exempt Goods:

Category | Specific Examples |

Agricultural Produce | Fresh fruits, vegetables (including potatoes, onions, tomatoes), food grains (wheat, rice, cereals), pulses, unprocessed spices (including cardamom, cloves, black pepper), flowers, leaves (including betel leaves), seeds (including oilseeds), fodder |

Livestock | Live animals (excluding horses meant for racing) including poultry (chicken, ducks), fish, worms (used for bait), silk cocoons, and their eggs |

Certain Food Items | Milk (excluding processed or flavored milk), curd, lassi, buttermilk, cheese (excluding processed cheese), honey, jaggery, agricultural implements (used for cultivating agricultural produce) |

Essential Supplies | Salt (excluding iodized salt), unbranded cereals (excluding breakfast cereals), educational supplies like maps, globes, and charts |

Textiles | Certain handloom fabrics (defined under the Handloom (Reservation of Articles for Production) Act, 2000), khadi (cotton fabric used for traditional Indian clothing) and khadi yarn, fibers like raw jute and silk waste |

Natural Resources | Uncut and unpolished diamonds, natural gas for domestic consumption |

Exempt Services:

Category | Specific Examples |

Healthcare | Services provided by a clinical establishment, diagnostic or pathological laboratory, for prevention, diagnosis, or treatment of illness, hospitalization, maternity, surgical operation, ambulance services (excluding those provided by a taxable person) |

Education | Services provided by an educational institution by way of teaching (including vocational training) provided to its students |

Financial Services | Long-term insurance policies (excluding unit-linked insurance plans), life insurance policies, basic banking transactions (excluding those provided by a taxable person) |

Religious and Charitable Services | Services provided by religious institutions in relation to religious rites or ceremonies; charitable activities for public welfare undertaken by a non-profit organization |

Public Transport | Services related to transportation of passengers by public transport vehicles like railways, buses, metros, taxis operated by a local authority, and public transportation by inland waterways |

Funeral Services | Services related to burials and cremations |

Detailed GST Rates on Commonly Used Items

The intricate fabric of the Indian market comprises a wide array of products consumed daily by millions. From groceries to gadgets, the GST imposed on these items affects the overall cost to the consumer. This section breaks down the GST rates on a selection of commonly used items, providing a comprehensive understanding that can guide consumers in their daily purchases.

Grocery and Food Items

The kitchen pantry and dining table of an Indian household showcase a variety of goods, some exempt from GST, while others attract a nominal rate aimed at minimal disruption to household budgets.

Table 1: GST Rates on Grocery and Food Items

Item | GST Rate |

Unprocessed cereals | 0% |

Milk | 0% |

Fresh fruits and vegetables | 0% |

Packaged and branded cereals | 5% |

Processed foods | 12% |

Dining out & takeaway food | 5%-18% |

Apparel and Textiles

Clothing and textiles, essential for basic human dignity and protection against the elements, carry GST rates reflective of the need to balance affordability with luxury.

Table 2: GST Rates on Apparel and Textiles

Item | GST Rate |

Garments under ₹1000 | 5% |

Garments over ₹1000 | 12% |

Synthetic yarn, fabric | 18% |

Apparel above ₹1000 | 12% |

Electronics and Appliances

In today's digital age, electronics and appliances are no longer luxuries but necessities for modern living. The GST rates on these items are structured to reflect their essential role.

Table 3: GST Rates on Electronics and Appliances

Item | GST Rate |

Mobile phones | 18% |

Laptops, computers | 18% |

Television sets | 18% |

Household appliances | 18%-28% |

Health and Personal Care

Health and personal care items, critical for maintaining hygiene and wellness, are taxed in a manner that seeks to ensure they remain accessible.

Table 4: GST Rates on Health and Personal Care

Item | GST Rate |

Medicines | 5%-12% |

Sanitary napkins | 0% |

Toiletries (soap, shampoo) | 18% |

Personal care appliances | 18% |

Historical Overview of GST Rate Changes

Key GST Rate Revisions and Rationale

Since the rollout of GST in July 2017, there have been several pivotal rate revisions intended to streamline the tax structure, stimulate economic growth, and address sector-specific challenges. One of the first major revisions involved lowering GST rates for over 200 items in November 2017, aiming to ease the burden on consumers and businesses adjusting to the new tax system. Another significant adjustment was the reduction of GST rates on housing projects to 5% and on affordable housing to 1% in March 2019, designed to boost the real estate sector and make housing more affordable.

Immediate Impact on Businesses and Consumers

Immediate responses to GST rate changes have varied across different sectors. For example, the reduction in GST rates for restaurants from 18% to 5% led to a temporary boost in consumer spending in the food services sector. However, the removal of the input tax credit for restaurants balanced out the impact on their profit margins. Similarly, the reduction in GST on consumer goods like washing machines and refrigerators from 28% to 18% in July 2018 led to a noticeable increase in consumer demand for these products.

Long-Term Economic Effects of GST Adjustments

The long-term economic effects of GST rate changes are complex and intertwined with other macroeconomic factors. However, certain trends are observable. The simplification and reduction of GST rates have generally been positive for consumer sentiment and spending, contributing to gradual economic growth. Furthermore, the input tax credit mechanism has incentivized businesses to enter the formal economy, enhancing tax compliance and broadening the tax base.

Assessing and Predicting Future GST Rate Changes

Economic Indicators and GST Rate Adjustments

The GST Council's decisions often reflect broader economic goals, such as stimulating growth or controlling inflation. For instance, during periods of economic slowdown, the Council might consider rate reductions to encourage consumer spending. Conversely, in times of robust growth, rate adjustments could focus on balancing revenue needs with sectoral incentives. Monitoring economic indicators like consumer price index (CPI), wholesale price index (WPI), and GDP growth provides insights into possible GST rate revisions.

Potential Sectors for Future GST Rate Adjustments

Emerging trends suggest several sectors could be in line for future GST rate adjustments:

- Healthcare and Education: There's ongoing debate about reducing GST rates or enhancing exemptions in these essential sectors to make services more accessible.

- Electric Vehicles (EVs) and Renewable Energy: To support environmental goals, further incentives in the form of reduced GST rates could be introduced, fostering growth in green technology sectors.

- Real Estate and Construction: Adjustments in GST rates in the real estate sector may continue, aimed at stimulating demand and addressing affordability issues.

The Role of Technology and Compliance in Future GST Rates

The increasing adoption of digital technologies in the GST compliance process is expected to have a dual impact. First, it may lead to more nuanced and sector-specific rate adjustments as the government gains better insight into economic activities. Second, improved compliance could result in revenue buoyancy, allowing for rate rationalization across various sectors without compromising tax revenues.

Expert Predictions on GST Rate Changes

Experts anticipate a cautious approach from the GST Council in the near term, with a focus on stabilizing the economy post-pandemic and addressing sector-specific challenges. There is a consensus that any future rate changes will likely aim to simplify the GST structure further, possibly reducing the number of slabs to make the system more efficient.

Predictions also include targeted incentives for sectors that align with national priorities, such as manufacturing under the "Make in India'' initiative, and sustainability projects. Enhanced compliance and digitization efforts are expected to facilitate these adjustments, making the GST system more dynamic and responsive to economic conditions.

Overview of the GST Composition Scheme

The Essence of the Composition Scheme

Introduced as a part of the GST framework, the Composition Scheme is a thoughtful provision aimed at supporting small businesses by simplifying tax compliance and reducing tax liability. Under this scheme, eligible businesses can pay GST at a fixed rate of their turnover, which is significantly lower than the standard rates. This approach not only eases the administrative burden but also aids in better cash flow management for small enterprises.

Eligibility Criteria for the Composition Scheme

The Composition Scheme is tailored for small businesses with an annual turnover threshold of up to Rs. 1.5 crore—Rs. 75 lakhs for special category states. The scheme is primarily available to manufacturers, traders, and restaurants (excluding those serving alcohol). Service providers, except for restaurants, were initially excluded but recent amendments have extended eligibility to a limited scope of service providers, further broadening the scheme’s appeal.

Benefits and Limitations of the Composition Scheme

Benefits:

- Reduced Tax Rates: Businesses pay GST at a nominal rate of 1% to 5%, depending on the nature of their operations.

- Simplified Compliance: Quarterly tax payments and annual returns reduce the compliance load.

- Improved Cash Flow: With lower tax rates, businesses can enjoy better liquidity.

Limitations:

- No Input Tax Credit: Businesses cannot claim input tax credit, which could be a deterrent for those with significant input taxes.

- Geographical Limitations: Businesses can only make intra-state sales, restricting their market reach.

- No E-commerce Sales: Composition dealers are prohibited from selling through e-commerce platforms.

Procedure for Opting into the Composition Scheme

Opting into the Composition Scheme involves a few straightforward steps:

- Eligibility Check: Businesses must first ensure they meet the eligibility criteria.

- GST Registration: If not already registered under GST, businesses must complete this step.

- Filing Form GST CMP-02: Businesses need to file this form on the GST portal before the start of the financial year for which they choose to opt into the scheme.

- Compliance Adjustments: Once opted in, businesses must adhere to the scheme's compliance requirements, including billing practices and tax payments.

The Composition Scheme represents a significant policy measure to support the small business sector in India, offering a pathway to simpler compliance and a lighter tax burden. By carefully evaluating the benefits and limitations, small businesses can make an informed decision on whether this scheme aligns with their operational model and financial strategies.

Navigating Tax Rates and Compliance Under the Composition Scheme

Tax Rates Under the Composition Scheme

The GST Composition Scheme offers significantly lower tax rates, typically ranging from 1% to 5%, depending on the business type:

- Manufacturers and Traders: 1% GST (0.5% CGST + 0.5% SGST) on the turnover of taxable supplies of goods.

- Restaurants not serving alcohol: 5% GST (2.5% CGST + 2.5% SGST) on the turnover.

- Other eligible service providers: 6% GST (3% CGST + 3% SGST) on the turnover of services.

These reduced rates allow businesses to lower their tax liability, enhancing their competitiveness and profitability.

Compliance Requirements for Composition Dealers

Composition dealers are required to maintain simplified records, issue bill of supply instead of tax invoices, and cannot charge GST from customers. They are also required to display "Composition taxable person" prominently at their place of business and on the bill of supply. Furthermore, they must file a quarterly return in Form GSTR-4 and an annual return in Form GSTR-9A, which simplifies the compliance process compared to regular taxpayers.

Impact of Non-Compliance

Failure to comply with the Composition Scheme's requirements can lead to penalties, including fines and disqualification from the scheme. Businesses found not eligible after opting for the scheme may be required to pay back the differential tax with interest. Continuous vigilance and adherence to the scheme's rules are imperative for availing its benefits without legal repercussions.

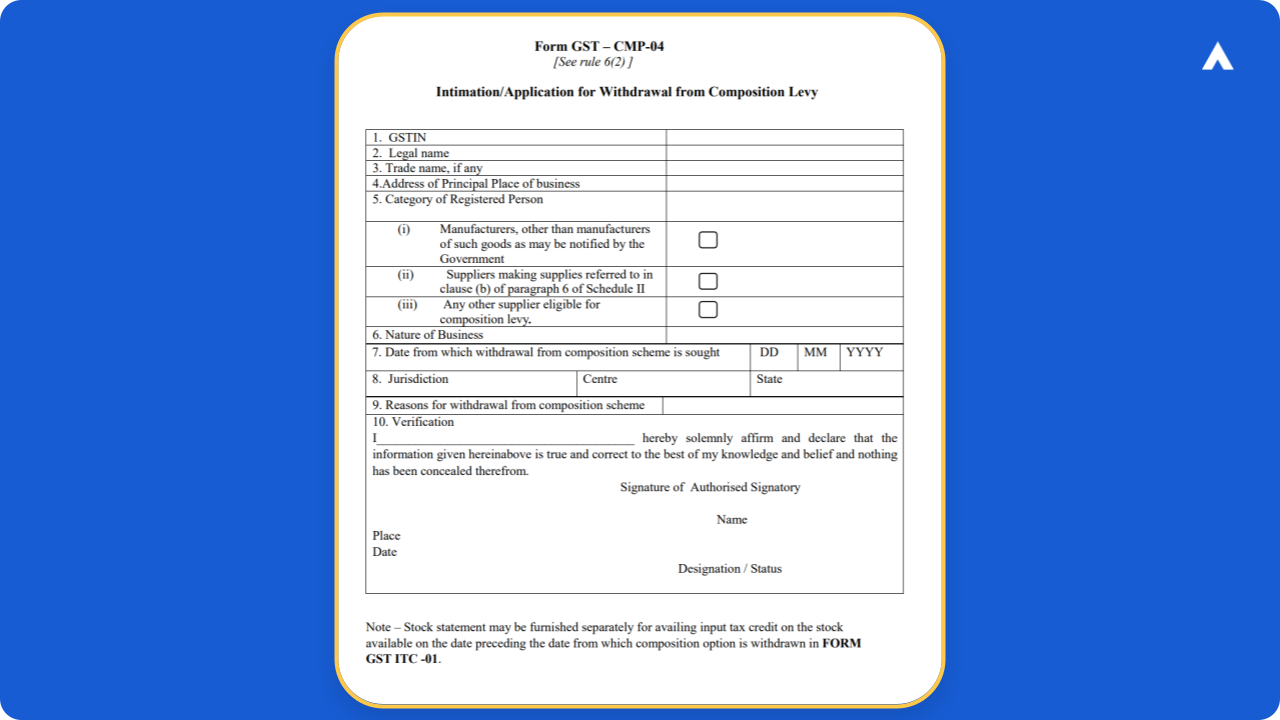

Transitioning Out of the Composition Scheme

Businesses may need to revert to the regular GST regime as they expand or if they wish to avail benefits like input tax credit. This transition requires filing Form GST CMP-04 and issuing a detailed stock declaration. The transition process is designed to be straightforward, allowing businesses flexibility in their tax compliance strategies as they grow and evolve.

The GST Composition Scheme presents a promising avenue for small businesses to simplify their tax obligations while benefiting from reduced tax rates. However, the benefits come with a responsibility to adhere to the scheme's compliance requirements and to regularly assess whether the scheme continues to serve the business's best interests as it grows and its operational dynamics change.

Understanding HSN Codes in the Context of GST

The Basics of HSN Codes

HSN codes, or Harmonized System of Nomenclature codes, represent a globally recognized system for classifying goods in international trade, developed by the World Customs Organization (WCO). These codes are designed to simplify the process of identifying goods across different countries, facilitating easier taxation, and customs procedures. In the context of India's GST, HSN codes serve as a critical tool for categorizing goods, ensuring uniformity and consistency in tax application across states and between different types of products.

HSN Codes and GST Rate Determination

Under the GST system, every product is assigned an HSN code, which determines the applicable tax rate based on predefined tax slabs (0%, 5%, 12%, 18%, and 28%). This classification system allows for a streamlined tax calculation process, enabling businesses and tax authorities to quickly identify the GST rates applicable to various goods. Accurate classification becomes a critical task for businesses, as the correct application of HSN codes directly impacts the GST levied on products, affecting pricing strategies, tax liability, and compliance status.

Compliance Requirements Related to HSN Codes

The GST legislation mandates businesses to declare HSN codes on their tax invoices and other relevant documentation, a requirement that underscores the importance of accurate goods classification. The level of detail required in the HSN classification (2, 4, or 8 digits) varies based on a business's turnover, with larger businesses required to provide more detailed codes. This requirement not only aids in the standardization of GST filing and compliance but also helps in streamlining the audit and verification processes, ensuring that businesses accurately account for their tax liabilities.

The integration of HSN codes into India's GST system represents a significant step towards simplifying the tax filing process, promoting greater transparency and ease of doing business. By understanding the basics of HSN codes, their role in determining GST rates, and the compliance requirements involved, businesses can better navigate the GST landscape, ensuring accurate tax reporting and minimizing the risk of non-compliance.

Navigating HSN Codes and Applying GST Rates

Finding the Right HSN Code for Your Products

Identifying the correct HSN code for products is a critical first step for GST compliance. Businesses can use the following resources and strategies to find the appropriate HSN codes:

- GST Council's Official Portal: The portal provides a comprehensive search tool allowing businesses to enter product descriptions or keywords to find corresponding HSN codes.

- HSN Code Finder Tools: Various online platforms offer HSN code lookup tools that simplify the search process by categorizing goods under different sections and chapters.

- Consulting with Tax Experts: For complex products or where ambiguity exists, consulting with a GST practitioner or tax expert can ensure accurate classification.

Common Goods and Their Corresponding GST Rates

Here's a simplified table illustrating common goods, their HSN codes, and the applicable GST rates to demonstrate how different products are categorized:

HSN Code | Description | GST Rate |

0204 | Meat of sheep or goats | 0% |

1001 | Wheat and meslin | 0% |

6109 | T-shirts, knitted or crocheted | 5% |

8517 | Mobile phones | 18% |

8703 | Cars and other motor vehicles | 28% |

This table offers a glimpse into the diverse range of goods covered under the GST regime and highlights the importance of accurate HSN code application.

Addressing Misclassification and Disputes

Misclassification of goods can lead to incorrect GST application, affecting a business's financial and compliance status. To address and rectify such issues, businesses should:

- Review and Update Product Classifications Regularly: Stay informed about changes in HSN codes or GST rates to ensure ongoing compliance.

- Maintain Detailed Documentation: Keep comprehensive records of how products are classified and the rationale behind the chosen HSN codes.

- Engage with GST Authorities: In case of disputes, proactively engage with GST authorities, providing documentation and reasoning to resolve classification issues.

Leveraging Technology for HSN and GST Compliance

Technological solutions play a pivotal role in simplifying HSN code management and GST compliance:

- GST Compliance Software: Many software solutions are equipped with built-in HSN code databases and GST rate calculators, automating the tax calculation process.

- Digital Record-Keeping: Utilizing digital tools for record-keeping not only aids in managing classifications and changes but also ensures readiness for audits and compliance checks.

Abhinandan Banerjee

(Associate Manager - Marketing)

Abhinandan is a dynamic Product and Content Marketer, boasting over seven years of experience in crafting impactful marketing strategies across diverse environments. Known for his strategic insights, he propels digital growth and boosts brand visibility by transforming complex ideas into compelling content that inspires action.