Get Personalised Solutions As Per Your Requirements

Connect with our sales team and get solutions to all your queries, alongside custom solutions for your needs.

GST Exemptions In India

Abhinandan Banerjee • February 5, 2026

The Goods and Services Tax (GST), implemented on July 1, 2017, marked a revolutionary change in India's indirect tax system. Unifying over a dozen of central and state taxes into a single tax system, GST aimed to eliminate the cascading effect of taxes, thereby simplifying tax administration and ensuring greater compliance.

GST: A Simplified Tax Structure

By integrating various indirect taxes under one umbrella, GST introduced a transparent and cohesive tax mechanism. It categorized goods and services into five primary tax slabs: 0%, 5%, 12%, 18%, and 28%. This simplification facilitated ease of doing business, contributing to a unified market across the nation.

The Broader Impact of GST Exemptions

GST exemptions have a multifaceted impact on the Indian economy and its consumers, influencing everything from the cost of living and business operations to broader economic growth and social welfare. This section explores these impacts and considers future directions for GST policy.

On Indian Economy and Consumers

- Enhanced Affordability and Accessibility: GST exemptions on essential goods and services directly contribute to their affordability and accessibility, ensuring that basic needs are met across all socioeconomic groups. This is crucial for maintaining social stability and promoting inclusive growth.

- Stimulation of Economic Activities: By exempting certain goods and services, the GST framework encourages consumption and helps stimulate economic activities in key sectors like agriculture, healthcare, and education. This, in turn, can lead to job creation and contribute to GDP growth.

- Challenges in Revenue Collection: While GST exemptions serve important social and economic objectives, they also pose challenges in terms of revenue collection for the government. Balancing the need for exemptions with the imperative of maintaining fiscal health is a continuous challenge.

Future Directions and Policy Recommendations

- Revisiting and Rationalizing Exemptions: As the Indian economy evolves, there's a need for periodic review and rationalization of GST exemptions. This involves assessing the continuing relevance of existing exemptions and considering new ones for emerging sectors.

- Enhancing the Efficiency of the GST Framework: Further simplification and clarification of the GST framework could help reduce compliance burdens, especially for small and medium-sized enterprises. Improving the input tax credit mechanism, especially for sectors like agriculture and healthcare, could enhance the overall efficiency of the GST system.

- Leveraging Technology for Better Compliance and Administration: The use of advanced technology can streamline GST compliance and administration, making it easier for businesses to adhere to regulations and for the government to monitor and collect revenue.

Clarifying GST Terms: Exemption, Nil-Rated, and Non-GST Supplies

Understanding the nuances of GST terminology is pivotal for businesses and consumers alike to navigate the tax landscape effectively. Here we delve into the distinctions among exempted, nil-rated, and non-GST supplies.

Definitions and Distinctions

- Exempted Supplies: These are goods or services on which GST is not levied. The key characteristic of exempted supplies is that input tax credit (ITC) cannot be claimed for the GST paid on inputs used to manufacture these goods or provide these services. This category primarily includes essentials that are vital for daily living and public welfare.

- Nil-Rated Supplies: Goods and services that are taxable under GST but have a tax rate of 0% fall under nil-rated supplies. Unlike exempted supplies, in the case of nil-rated supplies, businesses can claim ITC for the inputs used. This provision is designed to reduce the cost of essential goods and services, making them more accessible to the general populace.

- Non-GST Supplies: These are the goods and services that are outside the purview of GST and include items like alcohol for human consumption, petroleum products, and electricity. Since these are not covered by GST, no tax is levied, and consequently, ITC is not applicable.

Comparative Analysis

The primary difference lies in the eligibility to claim input tax credit. While nil-rated supplies allow for the claiming of ITC, exempted supplies do not. Non-GST supplies, being outside the ambit of GST, follow a different set of regulations altogether. Understanding these differences is crucial for businesses in planning their taxation strategies and for consumers to be aware of the tax implications of their purchases.

By clearly defining and distinguishing these categories, the GST framework aims to streamline tax administration and ensure a transparent tax mechanism, thereby facilitating compliance and ease of doing business.

Advantages of GST Exemptions

The GST exemptions, including nil-rated and non-GST supplies, confer significant benefits to both consumers and businesses, aligning with the broader economic objectives of growth, equity, and efficiency.

For Consumers

- Reduced Cost of Essential Goods and Services: By exempting or applying a nil rate of GST on essential goods and services, the government ensures that basic necessities are affordable for all sections of society. This not only aids in maintaining a low cost of living but also promotes equitable access to essential resources such as food, healthcare, and education.

For Businesses

- Impact on Operational Costs: Businesses dealing in exempted or nil-rated goods and services can benefit from reduced operational costs. While the inability to claim ITC on exempt supplies might seem like a disadvantage, the overall cost reduction in essential inputs and the increased demand for such goods and services can offset this impact. Additionally, for nil-rated supplies, the ability to claim ITC helps in reducing the cost of inputs, thus potentially lowering the price of the final goods or services.

- Encouragement of Certain Industries: GST exemptions are strategically used to encourage the growth of specific industries critical for the country’s development. For example, the agriculture sector benefits from exemptions on several inputs and services, supporting farmers and ensuring food security. Similarly, exemptions in the renewable energy sector promote sustainability and innovation in green technologies.

By carefully selecting goods and services for GST exemptions, the government not only protects the interests of the consumers, especially the economically vulnerable sections, but also fosters a conducive environment for businesses to thrive. These exemptions are instrumental in stimulating economic activity, promoting sectors of strategic importance, and achieving the broader goals of social welfare and sustainable development.

Comprehensive list of GST Exempt Services

Category | Examples of Exempted Services |

Health and Medical Services | Services by hospitals, nursing homes, and clinics. Medical services by doctors and paramedics. |

Educational Services | Pre-school education and education up to higher secondary school or equivalent. Services provided by the National Skill Development Corporation or Sector Skill Councils. |

Charitable and Religious Services | Services by entities registered under Section 12AA of the Income Tax Act for charitable activities. Services by a person by way of conduct of any religious ceremony. |

Agricultural Services | Services relating to agriculture by way of agricultural operations, supply of farm labor, and processes carried out at an agricultural farm. |

Government Services | Services provided by the Central Government, State Government, Union Territory or local authority, excluding certain specified services. |

Financial Services | Services by way of extending deposits, loans, or advances in so far as the consideration is represented by way of interest or discount. |

Transportation Services | Services by way of transportation of goods by road (excluding services of a goods transportation agency). Passenger transport services provided by a non-air-conditioned stage carriage. |

Insurance Services | Life insurance services provided under specified schemes like Janashree Bima Yojana, Aam Aadmi Bima Yojana, etc. |

Cultural and Sports Services | Services by way of admission to a museum, national park, wildlife sanctuary, tiger reserve, or zoo. Services by way of training or coaching in recreational activities relating to arts, culture, or sports. |

Public Utility Services | Services by way of collecting or providing news by an independent journalist, Press Trust of India, or United News of India. |

International Services | Services provided to the United Nations or a specified international organization. Services provided by an intermediary when the location of both the supplier and the recipient of goods is outside the taxable territory. |

Social Welfare Services | Services by an old age home run by the Government or by a charitable or religious entity. Services by way of public conveniences such as provision of facilities of bathroom, washroom, lavatories, urinal, or toilet. |

Entertainment Services | Services provided by a recognized sporting body for organizing sporting events. Services by way of sponsorship of sporting events organized by a national sports federation. |

Tourism Services | Services by way of a tour operator in relation to a tour conducted for a foreign tourist. |

The Agriculture Service Sector: A Case Study

- Overview: Agriculture, a pivotal sector of the Indian economy, has been significantly impacted by GST exemptions. Essential agricultural inputs like seeds, fertilizers, and machinery are either exempted from GST or subjected to a nil rate, aiming to reduce the cost burden on farmers.

- Impact Analysis: While the intention behind these exemptions is to support farmers, the inability to claim Input Tax Credit (ITC) on some exempt supplies could inadvertently increase operational costs. For instance, while fertilizers attract a 5% GST, farmers cannot claim ITC on it because the produce they sell is exempt from GST. This paradox has sparked a discussion on the need to refine the GST structure for agriculture to ensure that benefits fully percolate to the grassroots level.

- Expert Opinion: Economists suggest that a more nuanced approach, possibly including a reconsideration of the ITC mechanism for exempt sectors, could enhance the sector's productivity and contribute to higher GDP growth from agriculture.

- Impact on Farming Costs: By exempting agricultural supplies from GST, the government helps lower the operational costs for farmers. This is crucial for small and marginal farmers who operate on thin margins and are particularly vulnerable to price volatility in the market.

The Renewable Energy Service Sector: A Case Study

- Overview: The renewable energy sector has been identified as a key driver for sustainable development. GST exemptions and concessions for solar panels, wind turbines, and related services are intended to spur growth in this sector.

- Impact Analysis: The concessional GST rates have indeed lowered the cost of setting up renewable energy projects. However, challenges remain, such as the ambiguity in classifying certain renewable energy equipment under specified GST rates, leading to litigation and delays.

- Expert Opinion: Industry experts advocate for clearer guidelines and more comprehensive GST exemptions on ancillary services to ensure the seamless implementation of renewable energy projects. Such measures could accelerate India's transition to green energy, aligning with global sustainability goals.

The Healthcare Service Sector: Navigating GST Exemptions

The healthcare sector benefits significantly from GST exemptions, with a focus on making healthcare services more accessible and affordable to the public. Essential services provided by hospitals, clinics, and similar institutions are exempt from GST, alongside a list of critical medicines and healthcare equipment.

Impact Analysis

While exempting healthcare services from GST has undeniably made healthcare more affordable, the sector faces challenges, particularly regarding the input tax credit (ITC). Healthcare providers cannot claim ITC on the GST paid for inputs or input services, which might lead to an increase in operational costs and, indirectly, the cost of healthcare services.

Expert Opinion

Experts suggest a balanced approach, where critical inputs for healthcare services, especially those related to life-saving equipment and medicines, might be considered for lower GST rates or specific ITC provisions. This could help in offsetting the increased costs and ensuring that the benefits of GST exemptions are fully realized by the end consumers.

The Education Service Sector: The Impact of GST Exemptions

Education is another sector that enjoys GST exemptions, with the aim of promoting literacy and education across India. Services provided by educational institutions to their students, faculty, and staff are exempt from GST. This includes courses, examinations, and various types of training programs.

Impact Analysis

The exemption of educational services from GST underlines the government's commitment to education. However, like healthcare, the education sector cannot claim ITC on GST paid for their inputs, raising the cost of infrastructure development and educational materials. This has stirred discussions on finding a middle ground that supports the growth and quality improvement of educational services without imposing additional financial burdens.

Expert Opinion

Education sector analysts recommend reevaluating the GST framework to allow educational institutions to claim ITC on at least some critical inputs. This adjustment could potentially lower the overall costs of education and support the sector's expansion and modernization, especially in the adoption of digital learning tools and technologies.

Services Essential for Farming

In addition to supplies, various services crucial for farming, such as soil testing, warehousing, and transportation of agricultural produce, are also exempt from GST. These exemptions are designed to encourage the use of professional services that can enhance productivity and

reduce post-harvest losses, thereby increasing the overall efficiency of the agricultural sector.

- Enhancing Agricultural Productivity: The exemption of services essential for farming from GST lowers the cost of these services, making them more accessible to farmers. This, in turn, can lead to better crop management, higher yields, and increased profitability for farmers across the country.

The support for agriculture through GST exemptions is a testament to the government's strategic approach to nurturing this vital sector. By making essential supplies and services more affordable, the GST exemptions contribute significantly to the sustainability and growth of agriculture in India, ensuring food security and economic stability.

Transportation and Public Utilities

The exemption of certain transportation services and public utilities from GST is another measure aimed at easing the financial burden on the general populace and supporting economic activities.

Exempted Transportation Services

Transportation services for goods, where the gross amount charged is below a specified threshold, are exempt from GST. This exemption is particularly beneficial for small and medium-sized enterprises (SMEs) and promotes the seamless movement of goods across the country. Public transport services, including metro and local trains, are also exempt, making daily commute more affordable for millions of citizens.

- Impact on SMEs and Daily Commuters: The exemption of transportation services from GST facilitates a more economical transportation of goods, reducing costs for businesses and consumers alike. For daily commuters, the affordability of public transport is crucial for accessing employment and education, underscoring the social benefit of this exemption.

- Goods Transport Agency (GTA) Services: Transportation services provided by GTAs for goods are exempt from GST up to a certain freight charge limit. This exemption is aimed at supporting the logistics sector, especially benefiting SMEs that rely on these services for the distribution of goods.

- Courier and Parcel Services: Small consignments transported through courier or parcel services enjoy a GST exemption up to a specified value limit. This facilitates the movement of small-scale shipments without the additional burden of GST, promoting e-commerce and small businesses.

Public Utilities: Water, Sanitation, Electricity

Essential public utilities such as water supply, sanitation services, and electricity for residential use are exempt from GST. This measure ensures that basic utilities remain affordable, contributing to public health and well-being.

- Ensuring Access to Basic Needs: The exemption of public utilities from GST is a critical step in ensuring that all citizens have access to basic services necessary for a dignified life. It supports the government's goals of improving public health, hygiene, and ensuring energy security for its population.

The GST exemptions on transportation services and public utilities play a significant role in supporting economic activities and ensuring that basic services are accessible to all. These exemptions reflect the government's commitment to social welfare and economic development, aiming to create a mo re inclusive and sustainable future for India.

Comprehensive List of GST-Exempt Goods

Category | Exempted Goods |

Agricultural Products | Fresh, unprocessed fruits and vegetables |

Unprocessed cereals and pulses like rice, wheat, and dal | |

Fresh milk, fresh meat, and poultry | |

Unbranded wheat flour and gram flour | |

Fresh or chilled fish and other aquatic products | |

Dairy and Livestock | Fresh milk and certain dairy products |

Live bovine animals, swine, sheep, goats, poultry, and other live animals | |

Food Items | Natural, unbranded honey |

Prasad supplied by religious institutions | |

Unbranded salt (excluding iodized salt) | |

Health and Medical | Blood and blood components such as plasma and platelets |

Human organs for medical use | |

Contraceptives including contraceptive pills | |

Educational Items | Books, including Braille books |

Educational and technical stationery items | |

Textiles and Clothing | Khadi yarn, fabric, and garments |

Silk yarn and silk worm laying, cocoon | |

Religious and Cultural Items | Handicraft goods like wooden frames, artistic paintings, and other handmade items |

Puja samagri, rudraksha, and other items used in religious ceremonies | |

Miscellaneous | Non-air conditioned public transport vehicles |

Common salt (excluding branded salt) | |

Non-packaged drinking water | |

Charcoal used for household consumption |

Food and Agriculture Products

In recognizing the fundamental need for affordable and accessible food and agricultural products, the GST council has exempted several items in this category. This exemption covers a broad spectrum of goods, from staple food grains to vegetables and fruits, ensuring that the basic nutritional needs are met for all sections of the population.

- Grains and Cereals: Essential grains like rice and wheat carry a 0% GST rate, classified under specific HSN codes such as 1006 for rice and 1001 for wheat. These exemptions play a critical role in stabilizing food prices and ensuring food security.

- Fruits and Vegetables: Fresh fruits and vegetables are exempt from GST, promoting healthier lifestyle choices among the Indian populace. These items do not have specific HSN codes as they are unprocessed and considered natural agricultural produce.

Healthcare and Medicinal Supplies

The GST framework exempts several healthcare and medical supplies to make healthcare services more affordable and accessible. This includes life-saving drugs and equipment, underscoring the government's commitment to public health.

- Pharmaceuticals: Essential drugs used in treating various diseases, including lifesaving drugs, are exempt from GST. For instance, insulin (HSN code 3004) is tax-exempt, reflecting the intent to alleviate the financial burden on diabetes patients.

- Medical Equipment: Certain medical equipment crucial for patient care, such as hearing aids (HSN code 9021), is also exempt from GST, supporting the healthcare infrastructure.

Educational Materials and Services

To promote education and ensure that it is accessible to everyone, the GST council has exempted educational materials and services from the tax.

- Books and Periodicals: Printed books, including textbooks and journals that are essential for educational purposes, are exempt from GST. These items fall under various HSN codes, such as 4901 for printed books.

- Educational Services: Services provided by educational institutions, including tuition fees and examination fees, are exempt from GST, ensuring that education remains within the reach of every citizen.

Objectives Behind GST Exemptions

The primary objectives of GST exemptions are to ensure the affordability of basic necessities, support sectors critical to the nation's development, and promote social welfare. By carefully selecting goods and services for exemption, the policy aims to balance economic growth with the welfare of the most vulnerable sections of society.

Making Essential Items Affordable Through GST Exemptions

The strategic application of GST exemptions on essential goods and services is a deliberate move to ensure that basic necessities remain within financial reach for all layers of Indian society. This segment explores how exemptions impact the pricing of essential items and highlights real-life examples to demonstrate these effects in action.

Price Impact on Basic Necessities

GST exemptions directly influence the cost structure of essential goods and services by eliminating the tax component from their price. This not only makes such items more affordable but also helps in stabilizing prices in the market, protecting consumers from potential price volatility. Essential food items, healthcare services, and educational materials are notable beneficiaries of this policy, ensuring that the cost of living does not escalate beyond the reach of the average citizen.

- Example: The exemption of GST on grains and pulses directly benefits consumers by keeping the prices of these staple foods low, ensuring food security and nutritional access across socio-economic segments.

Case Studies: GST Exemptions in Action

To illustrate the tangible impact of GST exemptions, consider the healthcare sector, where life-saving drugs and healthcare services are exempt from GST. This decision has crucial implications for public health, making healthcare services and essential medications more accessible and affordable.

- Case Study: The exemption of GST on insulin and other critical diabetes management supplies significantly reduces the financial burden on millions of diabetes patients across India. By making these essential health items tax-free, the government aids in managing the long-term health condition more affordably.

Challenges in Administering GST Exemptions

While GST exemptions play a critical role in supporting economic and social welfare objectives, they also present certain administrative challenges, including the potential for evasion and misuse.

Potential for Evasion and Misuse

The exemption criteria can sometimes be exploited for tax evasion or misclassification of goods and services to avoid taxation. This not only leads to revenue loss for the government but can also create unfair competition among businesses.

- Example: Misclassification of non-exempt goods as exempt items is a common issue, requiring robust monitoring and enforcement mechanisms to counteract.

Balancing Act: Encouraging Compliance while Minimizing Abuse

Ensuring compliance with GST exemptions while preventing misuse requires a delicate balance. The government must continually refine exemption criteria, strengthen compliance mechanisms, and invest in taxpayer education to minimize abuse and optimize the benefits of GST exemptions.

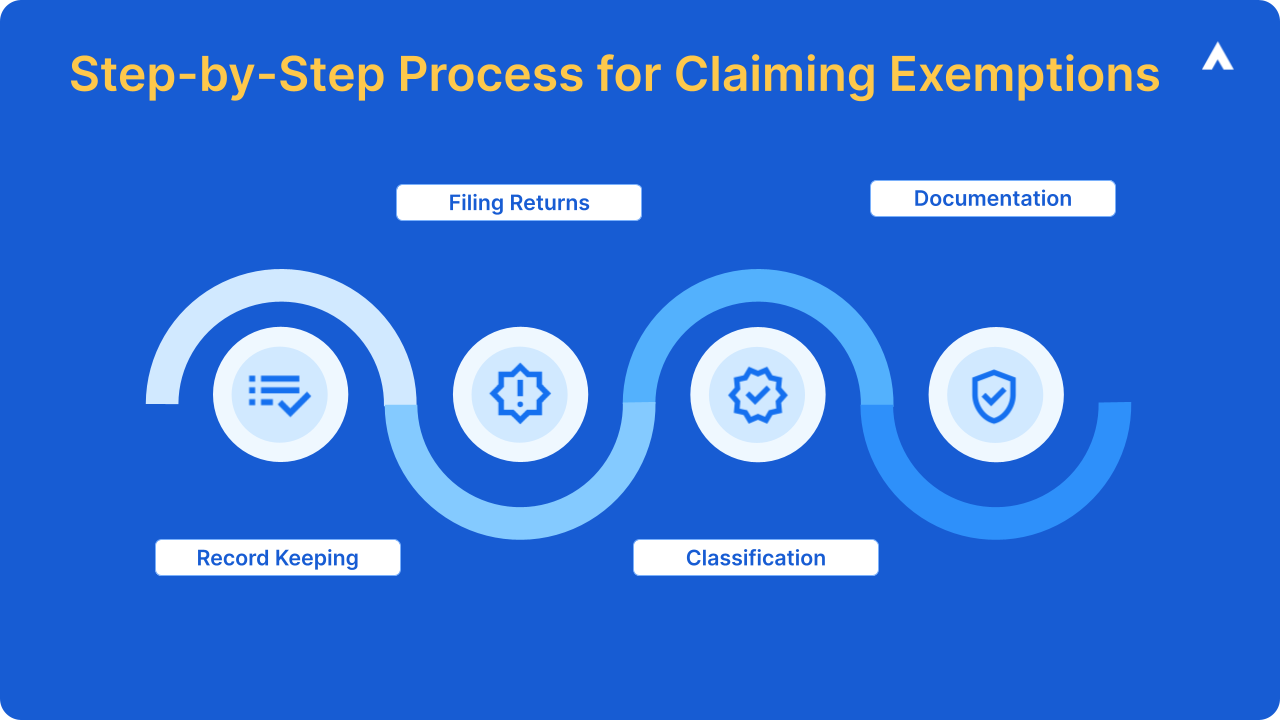

GST Exemption Procedures for Businesses

Understanding Eligibility and Documentation

For businesses operating in India, understanding the eligibility criteria for GST exemptions is paramount. Eligibility often depends on the nature of goods or services provided, with specific categories designated as exempt by the GST council. Documentation, including accurate classification of goods/services, tax invoices, and exemption certificates, forms the backbone of the exemption claim process.

- Key Documents: Businesses must maintain comprehensive records such as purchase invoices, exemption declarations, and corresponding HSN/SAC codes for the goods or services they're claiming exemptions on.

Step-by-Step Process for Claiming Exemptions

Claiming GST exemptions is a structured process that requires attention to detail and adherence to regulatory guidelines:

- Classification: Determine the correct HSN/SAC codes for your goods or services to verify if they fall under exempted categories.

- Documentation: Gather and prepare all necessary documentation, including evidence of exemption eligibility and transaction records.

- Filing Returns: While filing GST returns, report the exempted sales or services accurately, ensuring that the total value of exempt supplies is declared.

- Record Keeping: Maintain detailed records of all transactions related to exempt supplies, as they may be required for future audits or verifications by tax authorities.

Demystifying Common Misconceptions About GST Exemptions

Myth vs. Reality: Eligibility and Scope

One common misconception is that all goods or services related to education, healthcare, or agriculture are automatically exempt from GST. In reality, only specific items or services within these sectors qualify for exemptions, as detailed in the GST exemption list.

Clarifying the Impact on Input Tax Credit

Another area of confusion revolves around the input tax credit (ITC). Many businesses mistakenly believe they can claim ITC on inputs used to provide exempted goods or services. However, GST law stipulates that ITC cannot be claimed for inputs used in making exempt supplies.

Leveraging Technology for Simplifying GST Exemption Processes

Digital Tools and Platforms for Ease of Compliance

Technology plays a crucial role in simplifying the GST exemption process for businesses. Digital platforms like the GST portal offer tools for filing returns, tracking exemptions, and maintaining records, thereby facilitating compliance.

- GST Software Solutions: Many software solutions are designed to help businesses manage GST compliance more efficiently, including exemption claims.

FAQs on GST Exemption

1. What is GST Exemption?

GST exemption refers to the exclusion of certain goods and services from the purview of Goods and Services Tax (GST). This means that no GST is levied on the supply of these exempted goods and services.

2. Who is eligible for GST exemption?

Eligibility for GST exemption can vary based on the nature of the goods and services provided. Generally, businesses involved in the supply of essential goods and services like healthcare, education, and certain agricultural products are eligible for GST exemptions.

3. What types of goods are exempted from GST?

Goods typically exempted from GST include unprocessed food items, fresh fruits and vegetables, books, and certain handicraft items. The specific list of exempted goods may vary based on the latest notifications by the GST Council.

4. What types of services are exempted from GST?

Services that are commonly exempted from GST include healthcare services, educational services, services by the Reserve Bank of India (RBI), services provided by the government, and religious pilgrimage services.

5. How can I find out if a specific product or service is exempted from GST?

You can refer to the official GST website or the latest GST exemption notifications issued by the GST Council to check if a specific product or service is exempted from GST.

6. Do exempted goods and services need to be reported in GST returns?

Yes, even though exempted goods and services are not taxed, they still need to be reported in GST returns. Businesses must declare the value of exempt supplies in their GST returns.

7. What is the difference between nil-rated and exempted goods/services?

Nil-rated goods and services are those on which the GST rate is 0%, whereas exempted goods and services are entirely excluded from GST. Although both do not attract GST, they are categorized differently in GST returns.

8. Are exports exempt from GST?

Exports are generally zero-rated, meaning GST is not charged on exported goods and services. However, exporters can claim a refund of the input tax credit on the goods and services used in the production of exports.

9. Is registration mandatory for businesses dealing only in exempted goods and services?

Businesses exclusively dealing in exempted goods and services are not required to register for GST. However, if they deal in both exempt and taxable supplies, GST registration is mandatory.

10. Can input tax credit (ITC) be claimed on exempted supplies?

No, input tax credit cannot be claimed on inputs, input services, or capital goods used for making exempted supplies. ITC is only available for supplies that are taxable under GST.

11. Are there any threshold limits for GST exemption?

Yes, small businesses with an annual turnover below a certain threshold are exempt from GST registration. The threshold limit varies based on the type of business and the state in which it operates.

12. How often are GST exemption lists updated?

GST exemption lists are periodically reviewed and updated by the GST Council based on the needs and feedback from various stakeholders. It is important to stay updated with the latest notifications and amendments.

13. What should businesses do if they mistakenly charge GST on exempted goods or services?

If a business mistakenly charges GST on exempted goods or services, they must rectify the error by issuing a credit note to the customer and making the necessary adjustments in their GST returns.

14. What documentation is required to prove a GST exemption?

Businesses must maintain proper documentation, such as exemption certificates, contracts, and invoices, to substantiate the exemption claims in case of any audit or scrutiny by the tax authorities.

Abhinandan Banerjee

(Associate Manager - Marketing)

Abhinandan is a dynamic Product and Content Marketer, boasting over seven years of experience in crafting impactful marketing strategies across diverse environments. Known for his strategic insights, he propels digital growth and boosts brand visibility by transforming complex ideas into compelling content that inspires action.