Get Personalised Solutions As Per Your Requirements

Connect with our sales team and get solutions to all your queries, alongside custom solutions for your needs.

Advance Ruling Under GST: A Comprehensive Guide

Abhinandan Banerjee • February 5, 2026

Introduction to Advance Ruling

Concept and Importance

Advance Ruling is a legal mechanism in India that allows taxpayers to obtain a binding ruling on the tax implications of a proposed transaction before it is undertaken. This preemptive clarification helps in providing certainty, reducing litigation, and facilitating tax compliance. It is particularly valuable in complex transactions where the tax consequences are unclear.

Scope and Applicability

The scope of advance rulings extends across various tax domains, including income tax, indirect tax (such as GST), and transfer pricing. It is applicable to a wide range of taxpayers, including businesses, non-resident entities, and certain categories of residents, ensuring that a broad spectrum of tax matters can be addressed proactively.

Eligibility Criteria for Seeking an Advance Ruling

Eligible Applicants Across Tax Regimes

Advance rulings can be sought by different types of taxpayers, each subject to specific eligibility criteria determined by the respective tax laws:

- For GST: Manufacturers, service providers, and importers/exporters, among others, can seek advance rulings on GST-related queries.

- For Income Tax: Non-residents, certain residents, and Public Sector Undertakings (PSUs) can apply for rulings on income tax matters.

Specific Situations and Transactions

The eligibility to seek an advance ruling also depends on the nature of the transaction or the question posed. It typically covers issues related to the classification of goods and services, the applicability of tax rates, the determination of tax liabilities, and questions related to transfer pricing.

Types of Advance Rulings

Income Tax Advance Rulings

These rulings provide clarity on transactions involving income tax obligations, particularly for non-residents and PSUs, covering issues like income characterization, applicability of double taxation avoidance agreements (DTAAs), and determination of residential status.

Indirect Tax (GST) Advance Rulings

GST advance rulings help businesses understand the tax implications of their operations, including the classification of goods and services, applicability of tax rates, and input tax credit eligibility.

Transfer Pricing Advance Rulings

Transfer pricing rulings offer clarity on the pricing of transactions between associated enterprises across borders, ensuring that they are in compliance with arm's length principles and applicable transfer pricing rules.

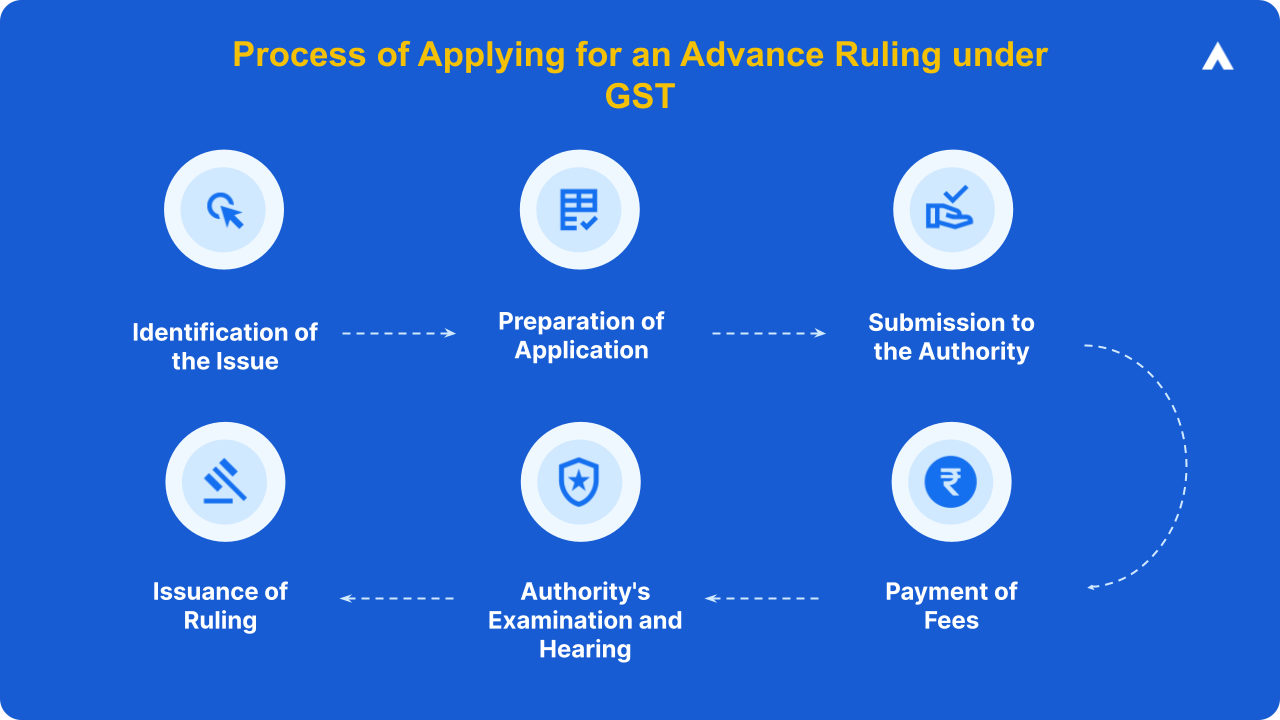

The Process of Applying for an Advance Ruling under GST

Applying for an advance ruling involves a systematic process that ensures taxpayers can seek clarification on tax matters with confidence and clarity:

- Identification of the Issue: The applicant must clearly identify the issue or transaction for which the advance ruling is sought, ensuring it falls within the scope of matters eligible for a ruling.

- Preparation of Application: The application should be meticulously prepared, detailing the question on which the advance ruling is sought, relevant facts, and the applicant's interpretation of the law.

- Submission to the Authority: Depending on the tax regime (income tax, GST, or transfer pricing), the application is submitted to the respective authority designated for handling advance ruling requests.

- Payment of Fees: A prescribed fee is payable at the time of application submission. The fee structure varies depending on the type of ruling and the applicant's category.

- Authority's Examination and Hearing: The advance ruling authority examines the application, conducts a hearing where the applicant and tax authorities can present their case, and then issues a ruling.

- Issuance of Ruling: The authority issues a written ruling on the matter, providing the applicant with legal clarity on the tax implications of the proposed transaction.

Documentation and Fees

The documentation required for an advance ruling application typically includes:

- A detailed description of the proposed transaction or issue.

- Relevant contractual agreements or draft agreements.

- Past precedents or rulings, if any, on similar issues.

- Any other supporting documents or explanations that help elucidate the matter.

The fee for applying for an advance ruling varies across tax domains:

- For GST: The fee is generally around INR 5,000 to INR 10,000, subject to changes by the GST council.

- For Income Tax: The fee structure can be more varied and is often based on the nature of the transaction and the applicant's status (e.g., resident vs. non-resident).

The Strategic Benefits of Obtaining an Advance Ruling

Ensuring Tax Certainty and Clarity

One of the foremost advantages of seeking an advance ruling is the tax certainty it offers businesses and taxpayers. In complex transactions, especially those involving new or innovative business models, the tax implications may not always be clear-cut. An advance ruling provides a legally binding decision from tax authorities on how tax laws apply to a specific situation, thereby eliminating ambiguity and enabling taxpayers to make informed decisions.

Reducing Tax Disputes and Litigation Risks

By clarifying the tax treatment of a transaction beforehand, advance rulings significantly reduce the potential for future disputes and litigation with tax authorities. This not only saves time and resources for both parties but also contributes to a more stable and predictable tax environment.

Process for Obtaining an Advance Ruling

Apply for advance rulings in GST for GST-registered people

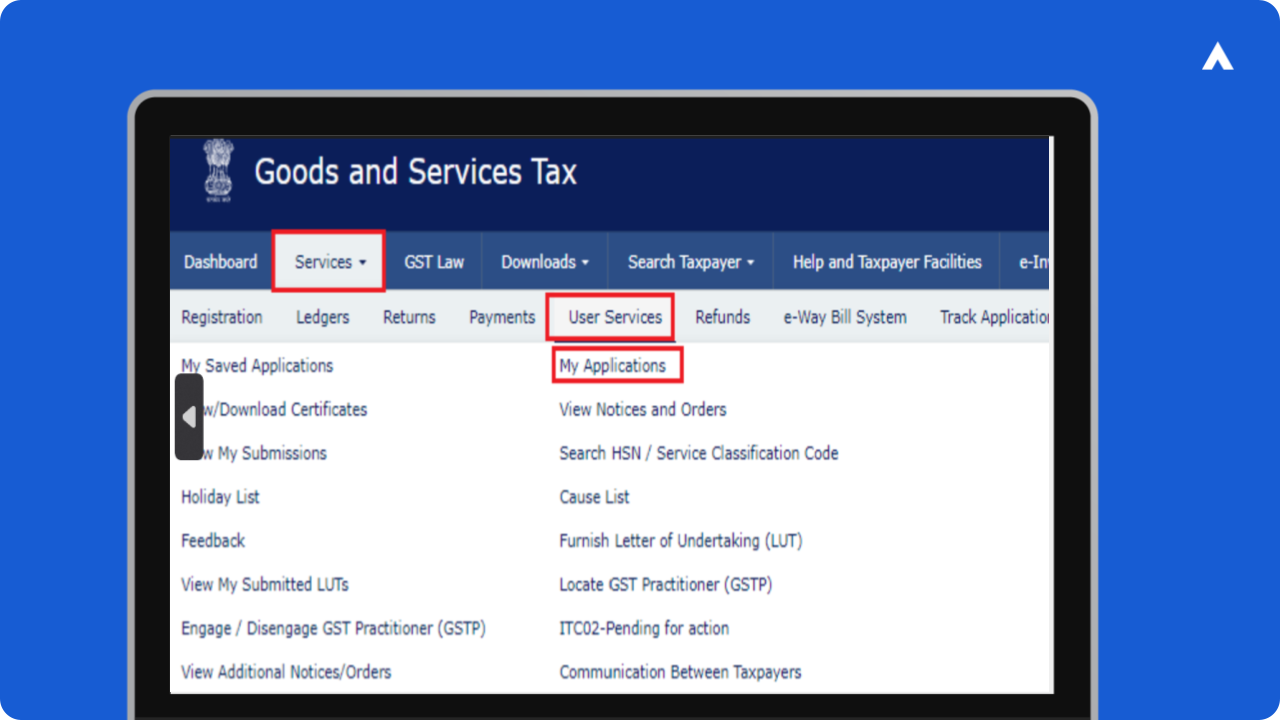

- Login to GST Portal

- Access the GST portal using your credentials and click on “My Applications” under 'Services > User Services'.

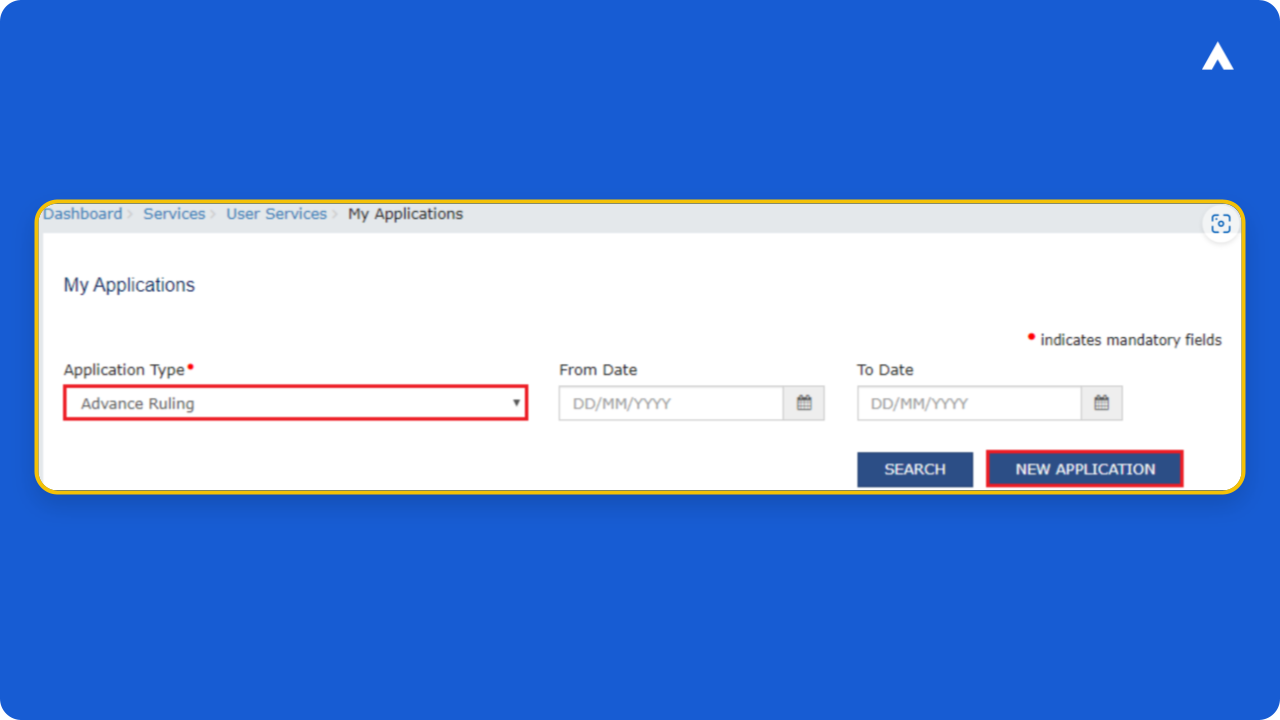

- Initiate New Application

- Select the application type as “Application for Advance Rulings.” Enter the from and to dates, and click on 'New Application.'

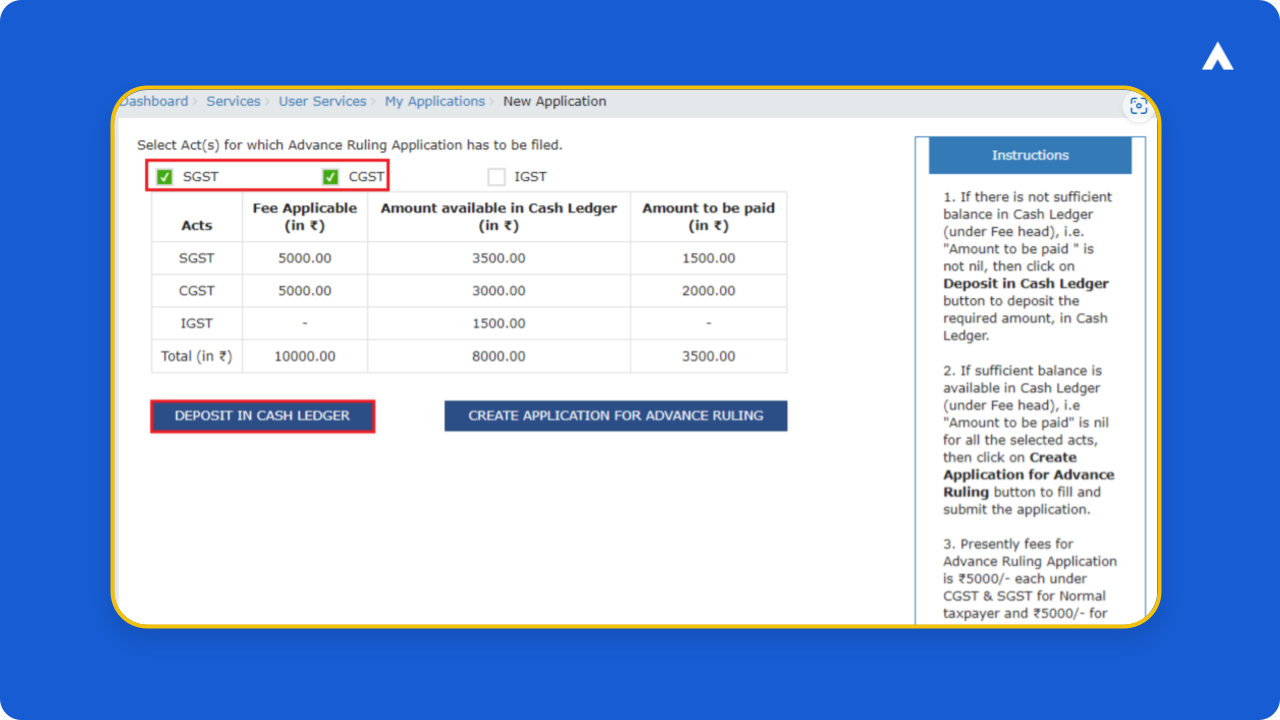

- Select the Relevant Act

- Choose the relevant act (CGST, SGST, or IGST). Deposit Rs.5000 under each act if necessary. If the amount is shown in the "Amount to be Paid" column, deposit it in the cash ledger.

- Pay the Fee

- Ensure the cash ledger has sufficient balance. Use net banking/e-banking, NEFT/RTGS, or OTC (Over the Counter) cash, demand draft, or cheque. Generate a challan, which will be created with a CIN upon successful payment. Click on 'Create Application for Advance Rulings.'

- Fill Out the Application Form

- Enter all required details, including:

- Correspondence address

- Nature of activity for which the advance ruling is needed

- Issues for which the advance ruling is sought

- Details of the advance ruling application

- Upload and attach supporting documents, provide a declaration, and complete verification.

- Review the Application

- Click on ‘Preview’ to review the details before submitting. The advanced ruling application PDF will be downloaded to your computer.

- Submit the Application

- File your application using either an EVC or DSC. Upon successful submission:

- The application fee is debited from the electronic cash ledger.

- An application reference number is generated.

- The application status changes to 'Filed.'

- An acknowledgment receipt is generated and can be downloaded.

- The applicant receives an SMS and an email confirmation.

Application Process for Advance Rulings in GST for Non-GST Registered People

- Obtain Temporary ID:

- Go to the GST portal and obtain a temporary ID by registering your details.

- Login to GST Portal:

- Use the temporary ID to log in.

- Create Challan:

- Generate a challan and pay the required fee.

- Download Application Form:

- Download and print the application form from the GST portal.

- Fill Out the Form:

- Complete the form with necessary details.

- Submit Application:

- Submit the filled form along with supporting documents to the state authority’s office.

Understanding the Timeframe for Receiving an Advance Ruling

While the timeframe for receiving an advance ruling can vary, authorities typically strive to issue rulings within a specific period from the date of application. For example, the GST advance ruling process aims to conclude within 90 to 120 days, although this can vary based on the complexity of the issue and the workload of the authority.

Several factors can influence how long it takes to receive an advance ruling, including:

- The completeness and clarity of the application submitted.

- The authority's current caseload and efficiency.

- The need for additional documentation or clarifications from the applicant.

The Financial Implications of Seeking an Advance Ruling

Government Fees for Application

The cost of obtaining an advance ruling in India varies depending on the type of ruling sought (e.g., GST, income tax, etc.) and the authority approached. Typically, government fees are set to cover the processing of applications and are structured to be accessible for all sizes of businesses seeking clarity on tax matters. For instance, the GST advance ruling application fee can range from INR 5,000 to INR 10,000, which is payable at the time of application submission. This fee is non-refundable, regardless of the outcome of the ruling.

Professional Fees for Preparation and Consultation

In addition to the government fees, taxpayers often incur professional fees for the preparation of the advance ruling application and for consultation. These fees can vary widely based on the complexity of the transaction in question and the expertise required to articulate the issue to the advanced ruling authority effectively. Engaging tax professionals or legal experts, who specialize in tax laws and have experience with advanced ruling applications, can significantly increase the chances of a favorable outcome but also adds to the overall cost.

The Legal Binding Nature of Advance Rulings

Advance rulings are legally binding on the applicant and the tax department in respect to the transaction for which the ruling was sought. This means both the taxpayer and the tax authorities must abide by the ruling, thereby providing legal certainty and minimizing disputes. However, it's crucial for applicants to understand that advance rulings are specific to the facts and circumstances presented at the time of the application.

Limitations and Exceptions: When Rulings May Not Apply

- While advance rulings offer a degree of certainty, there are limitations and exceptions to their applicability. For instance,

- if the law or the facts on which the ruling was based change after the ruling has been issued, the ruling may no longer be applicable.

- Additionally, advance rulings are not binding in cases where it is found that the facts or circumstances presented during the application were incomplete or misrepresented.

- Legal Precedent: In several cases, advance rulings have been revisited when subsequent legal amendments impacted the underlying basis of the ruling, showcasing the dynamic nature of tax law and the importance of keeping abreast with changes.

Challenging an Advance Ruling

The Legal Framework for Appeals

The ability to challenge an advance ruling is a critical aspect of India's tax regime, offering taxpayers recourse if they believe the ruling is flawed or adversely affects their interests. The legal framework for appeals varies across different tax jurisdictions but generally involves submitting an appeal to an appellate authority designated for advance rulings. This appellate body reviews the original ruling, considering new evidence or arguments to potentially overturn or modify the decision.

Grounds for contesting an advance ruling can include:

- Misinterpretation or misapplication of law by the authority.

- The discovery of new facts or evidence that was not considered in the original ruling.

- Procedural irregularities that affected the fairness or accuracy of the ruling.

When can one request for Advance Ruling under GST?

You can request a GST Advance Ruling in the following situations:

- Classification of Goods or Services: When you need to determine the correct classification of your goods or services under GST.

- Applicability of Notification: To clarify the applicability of a particular notification issued under GST law.

- Time of Supply: To determine the time when goods or services are considered supplied for GST purposes.

- Value of Supply: When you need to determine the value of goods or services for GST purposes.

- Admissibility of Input Tax Credit (ITC): To ascertain if input tax credit can be claimed on certain goods or services.

- Tax Liability: To determine whether a particular supply of goods or services is taxable and at what rate.

- Registration Requirement: To find out if you are required to register under GST.

- Nature of Activity: To determine if a specific activity amounts to a supply of goods or services under GST law.

- Exemptions: To verify if a supply of goods or services is exempt from GST.

Types of Advance Ruling Authorities under GST

Type of Advance Ruling Authority | Description |

Authority for Advance Ruling (AAR) | The initial authority where applications for Advance Ruling are filed. Comprises one member from the central tax and one member from the state tax. |

Appellate Authority for Advance Ruling (AAAR) | The authority to which appeals against the rulings of the AAR can be filed. Comprises one member from the central tax and one member from the state tax. |

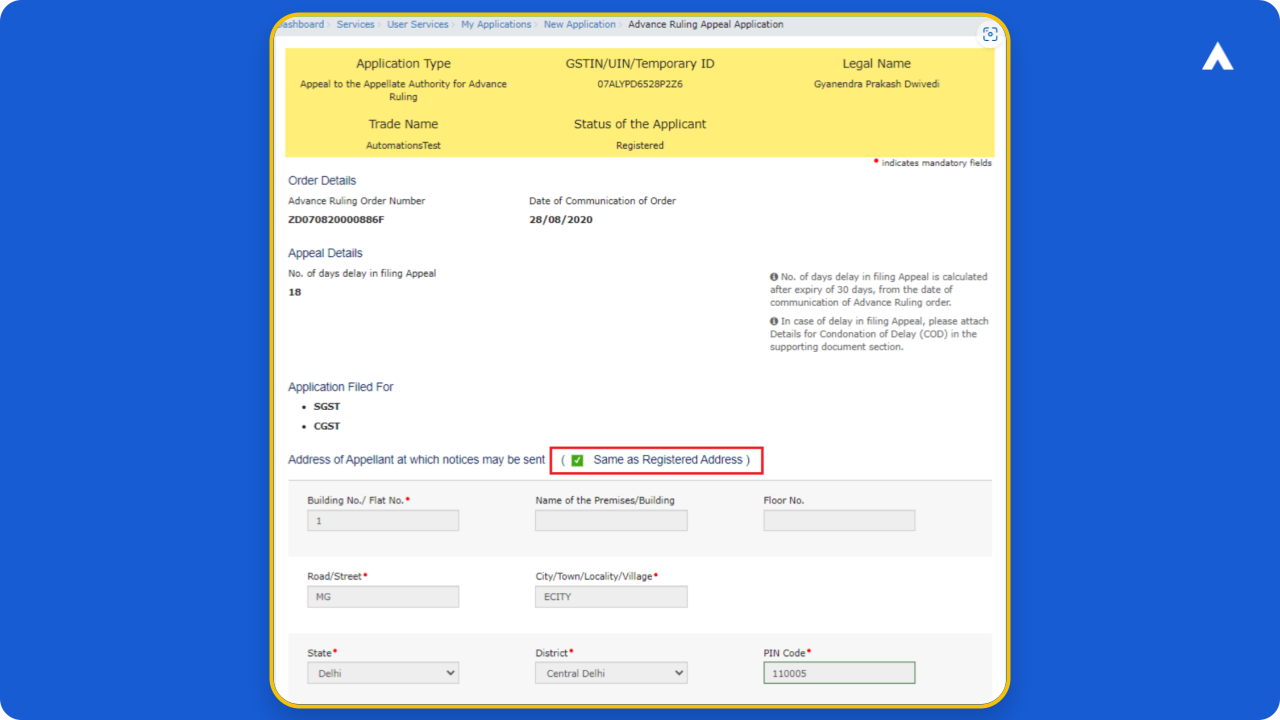

The Appeal Process for an Advance Ruling

- Access the GST Portal

Login to the GST portal using your credentials.

- Navigate to Appeal Filing

- Select "My Applications" under the services tab.

- Click on "File Appeal" against the relevant advance ruling.

- Fill Out the Appeal Form

- Choose the correct act (CGST/SGST/IGST).

- Provide details such as the ruling reference number, grounds for appeal, and any additional remarks.

- Attach Supporting Documents

Upload all relevant documents supporting your appeal, such as the original advance ruling, correspondence, and legal references.

- Pay the Appeal Fee

Generate and pay the required fee through the online payment gateway on the GST portal.

- Review and Submit

- Carefully review the filled-out appeal form and attached documents.

- Submit the appeal using Digital Signature Certificate (DSC) or Electronic Verification Code (EVC).

- Acknowledgment

Receive an acknowledgment receipt with an appeal reference number for future tracking.

- Hearing and Decision

- The appellate authority may schedule a hearing, where you can present your case.

- Await the decision, which will be communicated through the GST portal and other official channels.

Key Differences Between Advance Rulings and Tax Rulings

Legal Authority and Applicability

Advance rulings are issued by specialized bodies, such as the Authority for Advance Rulings (AAR), which have the authority to bind both the taxpayer who requested the ruling and the tax department. Tax rulings, however, are generally advisory and may not have the same binding effect on all taxpayers.

Scope and Subjects Covered

Advance rulings are typically limited to specific transactions and the parties involved in those transactions. Tax rulings have a broader application, providing guidance on the interpretation of tax laws that can affect a wide range of taxpayers and scenarios.

When will Advance Rulings not be allowed?

Pending Proceedings: If the question raised in the application is already pending in any proceedings before any officer, authority, tribunal, or court.

Decided Matters: If the question raised in the application has already been decided in any proceedings in the applicant's case.

Lack of Jurisdiction: If the application pertains to a matter that falls outside the jurisdiction of the Authority for Advance Ruling (AAR).

Incomplete Application: If the application is incomplete or does not comply with the prescribed format and fee requirements.

The Purpose and Impact of Advance Rulings

Certainty and Planning for Taxpayers

Advance rulings provide taxpayers with certainty about the tax treatment of proposed transactions, facilitating effective tax planning and decision-making. They are particularly valuable in complex transactions or when the tax law is ambiguous.

Influence on Legal and Business Strategies

By clarifying tax obligations in advance, these rulings enable businesses to structure their operations and investments in a tax-efficient manner, influencing broader legal and business strategies.

The Role and Significance of Tax Rulings

Guiding Tax Compliance and Interpretation

Tax rulings help in guiding taxpayers on how tax authorities interpret and apply tax laws to various transactions and scenarios, promoting compliance and reducing the likelihood of disputes.

Addressing Complex Tax Queries

Tax rulings provide a mechanism for taxpayers to obtain official clarification on complex tax queries, ensuring that their tax filing positions are in line with the authorities’ interpretations.

The Significance of Advance Rulings for Foreign Investors

Creating a Predictable Tax Environment

Advance rulings in India act as a beacon for foreign investors, illuminating the path of tax implications associated with potential investments. This clarity is paramount in a country known for its intricate tax laws and regulations. By securing an advance ruling, investors can forecast tax obligations with greater accuracy, allowing for more precise financial and operational planning. This foresight not only demystifies the tax landscape but also positions India as a more attractive destination for foreign capital, fostering an environment conducive to investment and growth.

Direct Benefits for Foreign Investors

The strategic advantages of obtaining an advance ruling are manifold:

- Risk Mitigation: By clarifying tax liabilities ahead of time, advance rulings significantly reduce the likelihood of future disputes with tax authorities, offering peace of mind to investors.

- Tax Planning: Armed with the knowledge of tax costs, investors can structure their investments more effectively, possibly taking advantage of tax efficiencies and optimizing returns on investment.

- Regulatory Transparency: The advance ruling process exemplifies India's commitment to enhancing its tax regulatory framework's transparency, making it easier for foreign investors to navigate the tax system.

Analyzing the Impact of Advance Rulings on Investment Decisions

Case Studies

Example 1: A European manufacturing company considering setting up a subsidiary in India sought an advance ruling regarding the applicability of GST on its inter-company services. The clarity provided by the ruling enabled the company to finalize its investment, confident in the knowledge of its tax obligations.

- Example 2: An American technology firm received an advance ruling on the tax treatment of its software licenses in India, influencing its decision to expand its operations within the country.

Expert Opinions on Investment Strategies

Experts suggest that advance rulings can serve as a critical component of an effective tax strategy for foreign investors. By proactively addressing potential tax issues, companies can avoid costly litigation and re-allocations of resources, ensuring a smoother operational runway in India. Moreover, the use of advance rulings is often seen as a best practice in tax risk management, recommended by advisors to their international clients contemplating investments in India.

Challenges and Considerations for Foreign Investors Seeking Advance Rulings

Navigating the Application Process

The journey to obtaining an advance ruling involves detailed preparation and understanding of the specific legal requirements. Foreign investors must meticulously document their proposed transactions and present a compelling case for the tax authority’s consideration. This process demands a thorough comprehension of the Indian tax landscape, often necessitating the guidance of local tax experts.

Understanding Limitations and Scope

It's imperative for investors to recognize that an advance ruling is not a one-size-fits-all solution; it is intricately tied to the specifics of the presented scenario. Changes in legislation or the factual basis of the transaction can render a ruling obsolete, necessitating a new analysis and potentially a fresh application for a new ruling. This dynamic aspect underscores the importance of continuous engagement with the evolving tax regulatory environment in India.

Avoiding Misuse of Advance Rulings

Recognizing Potential Areas for Misuse

Misuse of advance rulings can manifest in various forms, such as presenting hypothetical transactions to test tax avoidance strategies or withholding pertinent information that could affect the ruling. Such practices not only undermine the tax system's integrity but can also lead to legal repercussions, including penalties and revised tax obligations upon review.

Strategies for Ethical Application and Use

Applicants can employ several strategies to ensure the ethical use of advance rulings:

- Comprehensive Disclosure: Ensure all relevant facts, documents, and contexts of the transaction are fully disclosed to the authorities.

- Genuine Intent: Seek advance rulings only for transactions with a genuine business purpose, not for exploring potential tax evasion strategies.

- Consultation: Engage with ethical tax professionals who understand the importance of maintaining integrity in the advance ruling process.

The Interplay Between Advance Rulings and APAs

Defining Advance Rulings and APAs in Transfer Pricing

Advance Rulings provide clarity on tax implications for specific transactions before they occur, aiding in tax planning and compliance. In the realm of transfer pricing, they help determine the tax liability associated with cross-border transactions within an enterprise.

Advance Pricing Agreements (APAs) are formal agreements between a taxpayer and tax authority, or multiple tax authorities, defining the methodology for pricing intra-group transactions for future years. APAs aim to prevent transfer pricing disputes by establishing clear pricing mechanisms in advance.

Synergies and Differences: How They Complement Each Other

While both mechanisms aim to provide certainty, their approaches differ. Advance rulings are transaction-specific and can encompass a broad range of tax queries, including but not limited to transfer pricing. APAs, however, are solely focused on transfer pricing arrangements, offering a proactive approach to manage potential disputes by agreeing on pricing methodologies in advance.

FAQs on Advance Ruling under GST

1. What is an Advance Ruling under GST?

An Advance Ruling is a written decision given by tax authorities to an applicant on questions regarding the interpretation or applicability of GST laws. It helps taxpayers plan their activities in accordance with the law and avoid future disputes.

2. Who can apply for an Advance Ruling?

Any person registered under GST or any person with a desire to register under GST can apply for an Advance Ruling.

3. What types of questions can be addressed through an Advance Ruling?

Questions that can be addressed include:

- Classification of goods and services

- Applicability of a notification issued under the provisions of the Act

- Determination of time and value of supply of goods or services

- Admissibility of input tax credit

- Determination of the liability to pay tax on any goods or services

- Whether the applicant is required to be registered

- Whether any particular activity amounts to or results in a supply of goods or services

4. What is the procedure to apply for an Advance Ruling?

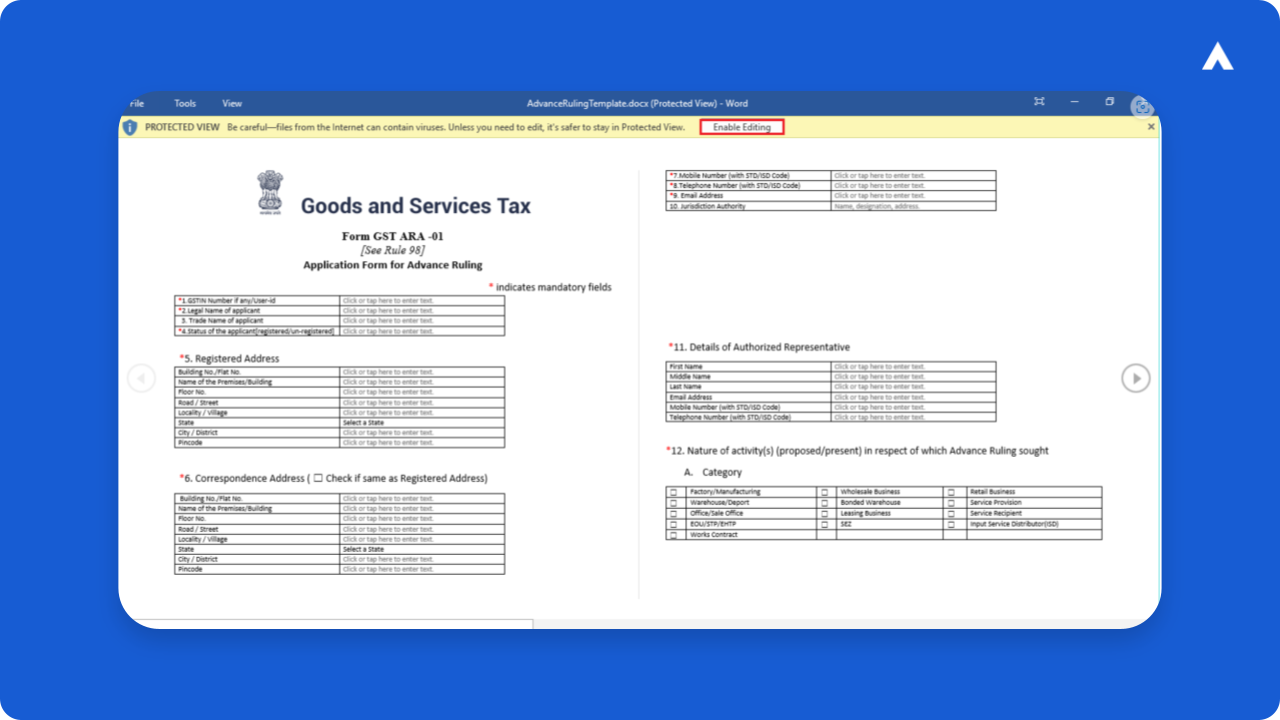

The applicant must submit Form GST ARA-01 along with the prescribed fee. The application can be filed online through the GST portal.

5. Who are the authorities that issue Advance Rulings?

Advance Rulings are issued by the Authority for Advance Ruling (AAR), which comprises one member from the central tax and one member from the state tax.

6. Is there an appeal process for Advance Rulings?

Yes, if an applicant or the tax authorities are not satisfied with the ruling of the AAR, they can appeal to the Appellate Authority for Advance Ruling (AAAR).

7. How long does it take to receive an Advance Ruling?

The AAR is required to pronounce its ruling within 90 days from the date of receipt of the application.

8. Is an Advance Ruling binding?

Yes, an Advance Ruling is binding on the applicant and the concerned officer or the jurisdictional officer in respect of the applicant. However, it is not binding on other taxpayers.

9. Can an Advance Ruling be withdrawn or modified?

An applicant can withdraw the application for Advance Ruling within 30 days from the date of application. However, once a ruling is given, it can only be modified or nullified by the courts.

10. What is the fee for applying for an Advance Ruling?

The fee for applying for an Advance Ruling is INR 5,000 for each question raised in the application.

11. What are the benefits of seeking an Advance Ruling?

Benefits include:

- Clarity on tax liability

- Minimization of litigation

- Certainty in tax treatment

- Proper planning of business activities

12. Can a non-resident apply for an Advance Ruling?

Yes, a non-resident taxable person can also apply for an Advance Ruling.

13. What happens if the Advance Ruling is not in favor of the applicant?

If the ruling is not in favor of the applicant, they have the option to appeal to the Appellate Authority for Advance Ruling (AAAR).

14. Are Advance Rulings publicly accessible?

Yes, Advance Rulings are published on the official GST website and are accessible to the public for transparency and guidance.

Glossary Terms

Category

Abhinandan Banerjee

(Associate Manager - Marketing)

Abhinandan is a dynamic Product and Content Marketer, boasting over seven years of experience in crafting impactful marketing strategies across diverse environments. Known for his strategic insights, he propels digital growth and boosts brand visibility by transforming complex ideas into compelling content that inspires action.