Introduction

From drug trafficking and organised crime to tax evasion and corruption, financial crime thrives when illegal proceeds are successfully disguised as lawful income. At the heart of this deception lies the practice of money laundering—a calculated process that allows criminals to obscure the origin of their wealth and reintegrate it into the mainstream economy.

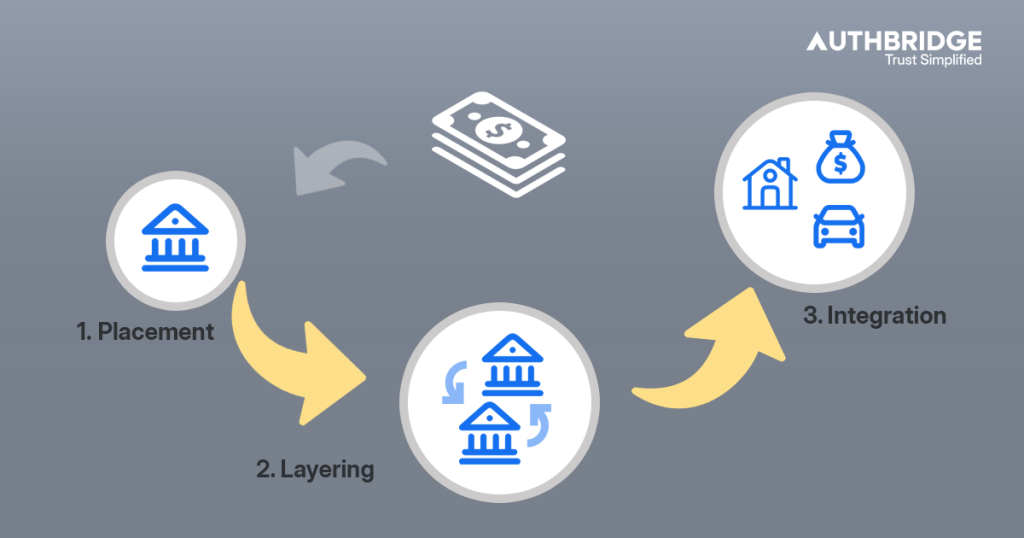

While the methods used may vary across regions, industries, and technologies, the laundering process typically follows a well-established pattern. Whether through shell companies, real estate investments, offshore accounts, or cryptocurrencies, criminals rely on a three-stage structure to move illicit funds: Placement, Layering, and Integration.

Each stage plays a distinct role in weakening financial oversight and concealing criminal footprints. Understanding these stages is essential not only for compliance professionals but also for policymakers, law enforcement, and financial institutions looking to disrupt the cycle before the funds are legitimised.

Money Laundering Stage 1: Placement

Placement is the first and most vulnerable stage of the money laundering process. It involves introducing illicit funds—typically large sums of cash—into the legal financial system. At this point, the money is most exposed to detection, making it a critical point for law enforcement and financial institutions to intervene.

Criminals seek to physically deposit or convert illegal cash into less suspicious forms while avoiding arousing attention. This may be done gradually in small amounts or through multiple entry points to avoid triggering regulatory thresholds or automated red flags.

Common Placement Techniques

Cash Deposits into Bank Accounts:

Depositing small amounts into multiple accounts—a method often referred to as smurfing or structuring—is used to avoid mandatory reporting limits. In many jurisdictions, deposits exceeding a certain threshold (e.g., ₹10 lakh in India or $10,000 in the US) must be reported.Purchasing High-Value Goods:

Illicit funds are sometimes used to purchase expensive items like luxury watches, cars, jewellery, or even artwork, which can later be sold and the funds reintroduced as clean money.Casino Transactions:

Criminals may buy chips with dirty money, gamble minimally, and then cash out the chips, claiming the funds as gambling winnings.Real Estate Down Payments or Rentals:

Placing illegal funds into real estate—either as deposits or rental payments—is another way to gain initial legitimacy.

Why Placement Is High Risk

This stage presents the highest risk for criminals because the source of funds is still directly traceable to criminal activity. As a result, financial institutions play a crucial role in identifying suspicious deposits, cash-heavy transactions, or patterns that deviate from a customer’s known profile. Tools such as cash transaction reports (CTR) and suspicious transaction reports (STR) are instrumental in detecting anomalies at this stage.

Money Laundering Stage 2: Layering

Once illicit funds have been successfully placed into the financial system, the second stage—Layering—begins. This phase is designed to obscure the origin and ownership of the money by creating multiple layers of financial transactions that make tracing the source exceedingly difficult for investigators.

Layering is essentially a game of deception. The goal is to move funds through a series of complex, often international transactions, which can include converting money into different currencies, transferring it between multiple accounts, and engaging in elaborate trades—all with the intent of breaking the audit trail.

Common Layering Techniques

Wire Transfers Across Jurisdictions:

Criminals often transfer funds between accounts in different countries, especially those with relatively lenient AML regulations. These transfers are structured to avoid raising suspicion and to exploit gaps in cross-border enforcement.Use of Shell Companies and Front Businesses:

Fake or inactive companies with minimal operations may be used to issue fictitious invoices, enabling illegal funds to move under the guise of legitimate business transactions.Investing in Securities or Commodities:

Purchasing and quickly reselling financial instruments or precious metals provides a way to further mask the money trail.Converting Funds into Cryptocurrencies:

Cryptocurrencies such as Bitcoin and Monero offer an added layer of anonymity and are increasingly used to shuffle funds beyond the reach of traditional oversight.

The Complexity Of Detection

Layering is deliberately complex. Unlike placement, which deals with physical cash, layering operates within digital financial systems—often in real time—making it harder to detect. Financial institutions must rely on behavioural analytics, AI-driven transaction monitoring, and cross-border data collaboration to uncover suspicious movement.

Moreover, because layering often mimics legitimate international business behaviour, compliance teams must be adept at spotting inconsistencies in transaction purpose, volume, frequency, and counterparty details.

Money Laundering Stage 3: Integration

Integration is the final stage in the money laundering process, where illicit funds re-enter the legitimate economy in a manner that makes them appear legally earned. At this point, the laundered money is typically indistinguishable from legitimate income, allowing criminals to use it freely for investment, business expansion, or personal enrichment.

This stage is the culmination of successful placement and layering. If both prior stages are executed without detection, the proceeds are now fully assimilated into the financial system—posing the greatest threat to economic and institutional integrity.

Common Integration Techniques

Investment in Real Estate or Businesses:

One of the most popular methods of integration involves purchasing property or injecting capital into legitimate businesses. These assets can then generate genuine revenue, further masking the origin of the initial funds.Lending Schemes or Loans to Self-Controlled Entities:

Criminals may loan the cleaned money to their own businesses or associates, creating a paper trail that justifies the funds as legitimate earnings or debt repayments.Luxury Asset Acquisitions:

At this stage, individuals may buy high-end items—artwork, luxury vehicles, yachts, or jewellery—using money that now carries a clean paper trail.Fake Contracts and Salary Payments:

Another tactic involves setting up sham employment or consultancy arrangements, wherein the criminal receives regular “salary” payments that originate from the laundered funds.

Why Integration Is So Dangerous

By the time money reaches the integration stage, its criminal origin is often obscured beyond recognition. Traditional compliance systems may struggle to detect anything unusual unless previous red flags were raised and investigated. As a result, proactive monitoring, continuous due diligence, and retrospective transaction audits are essential for spotting patterns even after integration has occurred.

This is also where tax evasion, insider trading, and political corruption often intersect with money laundering—making it crucial for banks and regulators to scrutinise the financial activities of high-net-worth individuals, politically exposed persons (PEPs), and businesses with opaque financial flows.

Conclusion

Money laundering is not a random act—it is a structured, multi-phase process that allows criminals to embed illicit wealth within the global economy. Each of the three stages—Placement, Layering, and Integration—plays a vital role in disguising the origins of illegal funds and enabling them to re-enter legitimate financial channels.

For banks, regulators, and compliance professionals, understanding these stages is more than a theoretical exercise; it is the foundation for building effective Anti-Money Laundering (AML) frameworks. Intervening early—especially during the placement stage—can dramatically reduce the chance of financial crime success. However, it is equally critical to detect and investigate layering tactics and integration signals, which often go unnoticed in the absence of sophisticated analytics and continuous monitoring.

With financial crimes becoming more advanced and decentralised, especially through the use of cryptocurrencies, shell entities, and cross-border layering techniques, institutions must evolve their AML capabilities. This includes not only leveraging AI and behavioural analytics but also strengthening due diligence, data integration, and reporting mechanisms.

The more deeply financial institutions understand how money laundering works, the better equipped they will be to disrupt it—protecting the integrity of the financial system and supporting broader efforts to combat organised crime.