Understanding The Concept Of A Money Mule

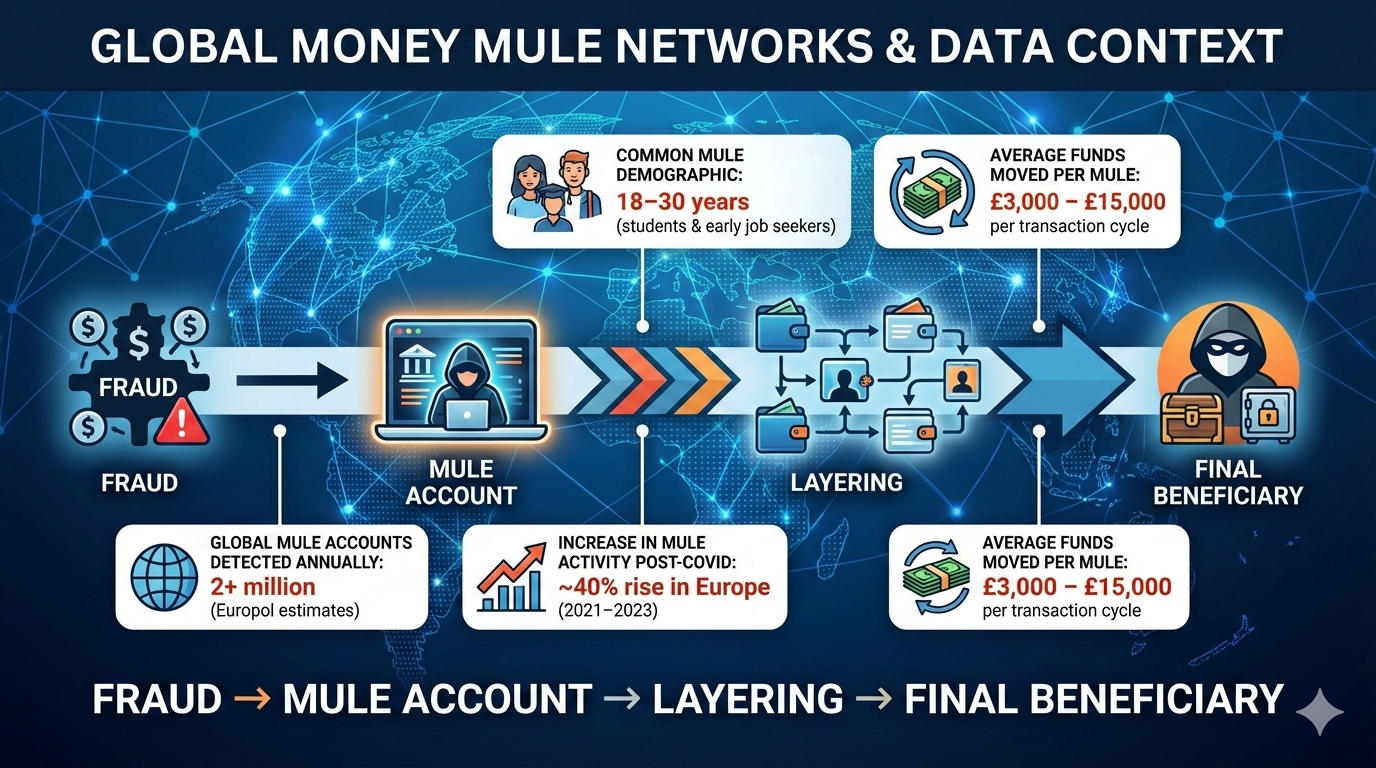

A money mule is an individual who is used—knowingly or unknowingly—to transfer, move, or launder illegally obtained money on behalf of criminals. The term “mule” is deliberately used to describe the role played: acting as a carrier that enables illicit funds to pass through legitimate financial systems without immediately alerting authorities.

In modern financial crime, money mules sit at the centre of fraud, cybercrime, identity theft, romance scams, and organised laundering networks. Criminals exploit personal bank accounts, digital wallets, and payment apps belonging to mules to distance themselves from the original crime. Once funds pass through a mule’s account, tracing the true beneficiary becomes significantly harder for banks and law enforcement agencies.

What makes money mule activity particularly dangerous is that many individuals do not realise they are participating in a crime. Students, job seekers, gig workers, and even professionals are frequently targeted using seemingly legitimate offers such as “payment processing jobs,” “work-from-home opportunities,” or requests from online acquaintances. According to Europol, money mule networks are now one of the most common operational tools used by organised crime groups to move funds across borders while avoiding detection.

From a regulatory perspective, money mule activity is treated as financial crime facilitation. Even if the individual claims ignorance, the legal system often views confirmed mule behaviour as a breach of anti-money laundering (AML) laws. This places individuals at risk of frozen accounts, criminal charges, long-term credit damage, and permanent restrictions from banking services.

Common Red Flags That Indicate Money Mule Risk

Money mule scams often rely on speed, secrecy, and confusion. While the methods may vary, the warning signs tend to be consistent across cases. Recognising these red flags early can help individuals avoid unintentionally participating in financial crime and facing serious legal or financial consequences.

Key Red Flags To Watch Out For:

Unexpected Job Offers Involving Money Transfers

Roles that ask you to receive, move, or “process” money using your personal bank account, especially without interviews or formal contracts.Promises Of Easy Or Guaranteed Income

Offers that claim high earnings for minimal effort, often framed as “part-time,” “remote,” or “work-from-home” opportunities.Requests To Use Your Bank Account Or Payment App

Any instruction to share account details or allow funds to pass through your account on behalf of someone else.Pressure To Act Quickly Or Maintain Secrecy

Being told to transfer money immediately or not to discuss the transaction with your bank, employer, or family.Vague Or Inconsistent Explanations About Fund Sources

Unclear reasons for why the money is being transferred, frequently changing stories, or evasive answers when questioned.Payments Originating From Unknown Or Overseas Accounts

Receiving funds from unfamiliar individuals, businesses, or international sources without a clear commercial relationship.Instructions To Convert Funds Into Cash Or Cryptocurrency

Requests to withdraw cash, buy gift cards, or transfer money into crypto wallets shortly after receipt.Communication Through Informal Channels Only

Reliance on messaging apps or social media instead of official email addresses or verifiable company domains.

Legal And Financial Consequences Of Being A Money Mule

Being linked to a money mule account can have serious and long-lasting consequences, even when the individual claims they were unaware of the criminal activity. Financial institutions and regulators typically treat mule activity as a material compliance breach, because such accounts directly facilitate fraud and money laundering.

From a banking perspective, the most immediate impact is account action. Once suspicious mule-like behaviour is detected, banks may freeze the account, restrict withdrawals, and reverse transactions under investigation. In many cases, the account holder is permanently barred from reopening accounts with the same bank, and adverse internal risk markers may be shared across the banking ecosystem. This can make it extremely difficult for individuals to access basic financial services in the future.

On the legal side, money mule activity may attract scrutiny under anti-money laundering (AML) and fraud prevention laws. Even if the person did not initiate the original scam, transferring or holding illicit funds can be interpreted as aiding or abetting financial crime. Law enforcement agencies often begin investigations from mule accounts because they represent the first identifiable touchpoint in an otherwise anonymous crime chain. As highlighted by multiple financial institutions, ignorance of the crime is not always accepted as a defence once repeated or high-value transactions are involved.

The financial consequences can also be severe. Funds credited into mule accounts are frequently clawed back once identified as proceeds of crime, leaving the account holder liable for negative balances or repayment obligations. Additionally, individuals may lose legitimate savings if accounts are frozen during extended investigations. According to industry reports, mule account holders often face credit score deterioration, impacting loan eligibility, employment background checks, and even rental agreements.

Long-Term Impact Of Money Mule Involvement

While legal action and immediate financial losses are the most visible outcomes of money mule involvement, the long-term impact often extends much further, affecting an individual’s professional life, digital footprint, and access to essential financial services. These consequences are rarely discussed upfront but can be far more damaging over time.

Key Long-Term Impacts

Permanent Banking Restrictions

Individuals linked to mule activity may be flagged internally by banks, leading to account closures and long-term difficulty in opening new savings, current, or salary accounts. In some cases, access to digital banking and payment platforms is also restricted.Negative Credit And Financial History

Suspicious account activity can impact creditworthiness, making it harder to secure loans, credit cards, or financial products in the future—even if no criminal conviction occurs.Employment And Career Risk

Background checks conducted by employers, especially in BFSI, fintech, consulting, or compliance-heavy roles, may surface adverse financial behaviour. This can result in job offer withdrawals or termination.Ongoing Regulatory Monitoring

Once flagged, individuals may be subjected to enhanced scrutiny for future transactions, including frequent KYC reviews, transaction delays, or reporting to regulatory bodies.Reputational And Digital Footprint Damage

In some cases, involvement in financial crime investigations may appear in public records, court documents, or employer verification databases, creating long-term reputational risk.Psychological And Social Impact

Victims of mule scams often experience stress, anxiety, and loss of trust in financial systems—particularly when they were unaware of their involvement initially.

Conclusion: Why Awareness of Money Mule Risks Matters More Than Ever

Money mule activity is no longer a niche or distant financial crime issue; it is a mainstream risk that affects individuals, banks, fintech platforms, employers, and the wider financial ecosystem. As fraudsters increasingly rely on real people and real bank accounts to move illicit funds, the boundary between victim and participant becomes dangerously thin. What often begins as an innocent job offer, a favour for an online acquaintance, or a quick way to earn extra money can quickly escalate into account freezes, long-term financial exclusion, and legal scrutiny.

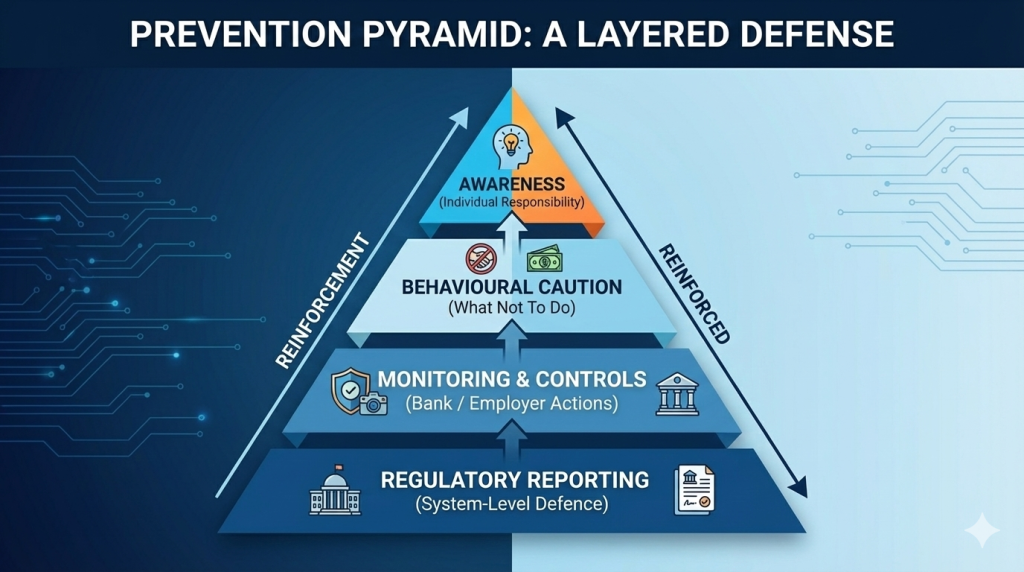

From an individual’s perspective, the most effective protection lies in awareness and caution. Understanding how money mule schemes operate, recognising suspicious requests involving bank accounts or transfers, and questioning offers that bypass normal employment or payment processes can prevent irreversible consequences. For organisations and financial institutions, the challenge is equally significant. Robust onboarding checks, continuous transaction monitoring, behavioural analytics, and timely customer education are no longer optional; they are foundational to effective AML and fraud prevention strategies.

Ultimately, combating money mule networks requires a shared responsibility. Regulators, banks, businesses, and customers all play a role in disrupting these schemes. By staying informed, vigilant, and sceptical of anything that feels unusually urgent or lucrative, individuals can protect themselves while contributing to a safer and more transparent financial system.